For a good deal of the last 18 months, investors yawned at our cautiousness and reluctance to chase stocks higher. For almost every stock that we wrote about, we had a buy under price that was well under the current price.

In the case of Manulife Financial Corporation (NYSE:MFC), that perfect entry was under $17.00 back when we covered it in June 2021. Interestingly, the stock’s 52-week low was well under that at $16.65. Did we get long? We tell you why it dropped sharply and where our buy point currently stands.

Q1-2022

MFC’s Q1-2022 EPS came in at 77 cents. This was down 5% versus 2021 and missed all estimates which expected at least 80 cents in this quarter. Analysts were behind the curve in pricing in the rapid Asian slowdown towards the end of the quarter and are now busy chopping estimates for Q2 and Q3. Lockdowns in China will likely have a significant impact on sales but this is likely a case of deferring revenue rather than losing it altogether. Nonetheless, since the news came at the time of the most volatile period in the markets, it perhaps increased the selloff.

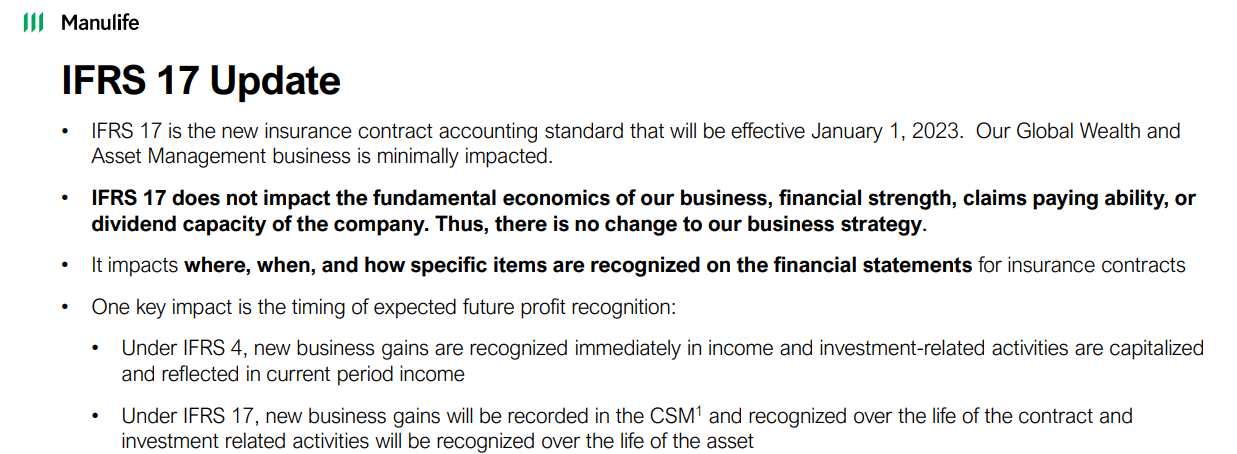

More problematic for MFC though was the disclosure on IFRS 17. As we have addressed this in the past, insurance companies have a huge asset base in relation to their tiny equity base. Those assets are invested to earn returns that help them meet or exceed their liabilities (read insurance payouts) over time. Valuing this is partially a science but to some extent is also an art. Well, we got a new artist in town and her name is IFRS 17.

Manulife IFRS 17 Update

MFC and other insurers under this standard in Canada, including Sun Life Financial (SLF) and Great-West Lifeco (OTCPK:GWLIF), have talked about this for some time. Everyone who followed this industry knew this was coming. Nonetheless, no one knew the exact impact until the individual company spelled it out. In the case of MFC, the impact appeared to be a little more than anticipated. The key points are below.

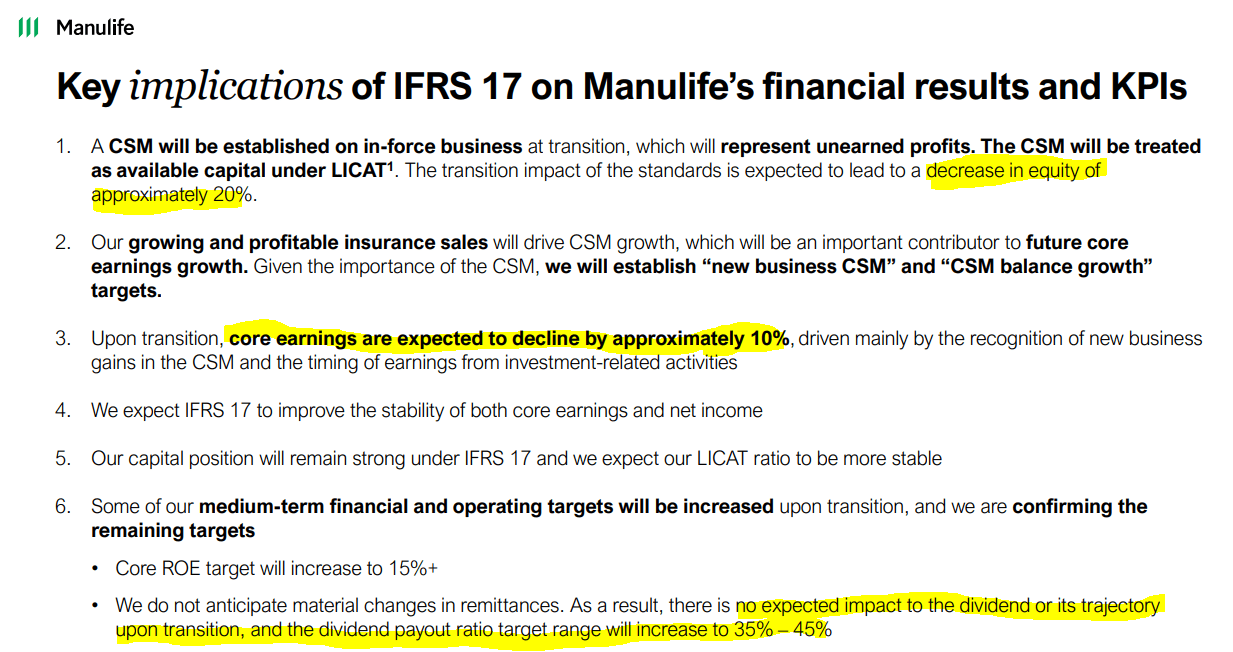

Manulife IFRS 17 Update

The decrease in equity is the decrease in tangible book value. If you remember, we base a lot of our insurance valuations on tangible book value, so that obviously is something we need to keep in mind as we set a price on this. Core earnings will also be knocked back by 10%. Dividends won’t change as per the company, but of course, a higher payout ratio might psychologically make the bull case less attractive.

Is This Bad?

From the point of a long-term shareholder, no, this is not bad news, at all. Gains that were being booked upfront now have to be recognized over the life of the contract. This standard exists in several forms across accounting. Even distribution is seen, for example, in straight line rents from REITs. Cash flow is lower than recognized revenue in the earlier years and higher than that in later years. Over time, things even out on both the balance sheet and income statement side.

Manulife IFRS 17 Update

The biggest worry investors should have is whether the changes would impact all the important LICAT ratios as equity is lowered. That answer is no. It won’t reduce LICAT ratios.

So not much changes here for MFC outside the traditional tangible book value number.

Valuation & Verdict

MFC is cheap compared to relative numbers for SLF and GWLIF.

We will note here that MFC’s LICAT ratio is higher than GWLIF’s (124%) and almost the same as that of SLF’s (143%) at 140%. This helps boost the case for MFC as it is not being priced lower due to higher relative risk.

On the US side, comparatives would likely include Prudential Financial, Inc. (PRU) and American International Group (AIG). MFC again stands out on the cheap side.

MFC also has the best dividend yield here, though it is close.

So our numbers tell us that is inexpensive, even though we have to still come up with a better way to use the new tangible book value numbers. One thing to consider though is that while all these examples look cheap, they have substantial risk in case of a massive reset of equity markets lower. There is an embedded return calculation placed on the insurance balance sheets, and earnings are likely to average lower if equity markets disappoint over the long term. That is precisely our thinking (0% total returns from S&P 500 (SPY) till 2030), and hence, we never went gung-ho on the name.

Our caution of not chasing this higher did pay off for us and our subscribers. We established our long position in January by selling the cash-secured puts $18 for June 2022. At the time, MFC was trading a bit higher.