Recession talks are increasing, and while we’re not in a recession, but rather, a bear market that is seeing a rally, this article provides investors with four stocks and tips for preparing for a potential recession.

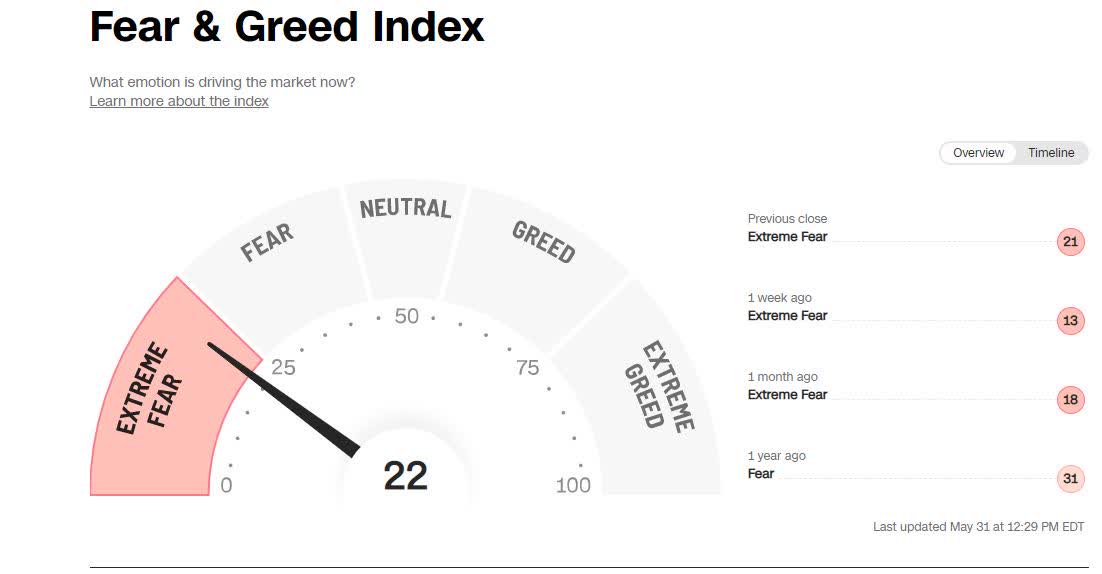

Soaring interest rates, high inflation, the war in Ukraine, and China’s economic slowdown create extreme fear in the markets, prompting investors to reconsider what they’re willing to pay for stocks. Big market swings are making clear that emotions are high, as indicated in the fear and greed index below. The Nasdaq has reached bear market territory, down 22.9% from its 16,057.44 November 19 peak. The Dow Jones is down nearly 10% YTD. And the S&P 500 has dropped more than 13% YTD, with its shortest and most recent bear market occurring during the pandemic from February 19, 2020, through March 23, 2020.

Fear and Greed Index (CNN Fear and Greed Index)

Because extremely low-interest rates acted like steroids for stocks and other investments throughout the pandemic, rising interest rates amid high inflation are creating a Wall Street withdrawal effect, prompting a significant slowdown across key variables, including an unexpected 1.5% Q1 GDP contraction, a continued battle with 40-year high inflation, and sticky variables like housing affordability and wages.

The Fed waited too long to tighten monetary policy, which they’ve tried to price to perfection to deliver a soft landing. A bumpy ride is perhaps more likely, as monetary policy and the lack of fiscal spending will create a drag on the economy, increasing the risk of recession. “Our goal, of course, is to get inflation back down to 2% without having the economy go into recession,” said Federal Reserve Chair, Jerome Powell. Despite some selling exhaustion in tech and new home sales (an indication that things are slowing), U.S. stocks appear to be bouncing back from the May-20th low. What investors may see as an opportunity could very well be a bear market rally – the bear’s greatest trick; convincing investors there is no bear so they invest, and then it’s too late. My former colleague and friend has the following to say about the current market environment.

Bottom line, our base case remains that last week’s strength will prove to be another bear market rally in the end…The turning point for the next leg of the bear may coincide with the next Fed meeting where it will likely be clear they are far from dovish…We stand by our call that the S&P 500 will trade close to 3400 by the end of 2Q earnings season – i.e., mid-August. – Mike Wilson, Morgan Stanley Strategist.

Given that we are experiencing a potential bear market rally, investors must be cautious that they do not invest prematurely.

The problem with making an assessment about the state of the economy today, based on current data points, is that these numbers are only ‘best guesses.’ Economic data is subject to substantive negative revisions as data gets collected and adjusted over the forthcoming 12- and 36-months. – Seeking Alpha Marketplace author Lance Roberts

How to Invest During a Recession

Typically, bear markets are not immediate. Many of the best days for Wall Street have occurred during a bear market, just prior to, or just after the end of one. The Dow Jones began rebounding on March 9, 2009, +20% from its 7924.56 low during the bear market of 2007-2009. The S&P 500 which was down 51.9% during that same period, surged 30% by mid-May 2009. The markets also experienced leaps and bounds following the shortest month-long bear market rally in 2020. What we experienced in 2020 is atypical, hence why it’s the shortest bear market ever achieved and exited.

Typically, bear markets are several months of downward pressure on equity markets with an offset with bonds. But, bonds have sold off in conjunction with equities due to rising rates and the uncertainty of monetary policy and its impact on monetary growth. As a result, we are seeing credit spreads and risks associated with corporate bonds.

While rates have increased, so has credit risk; this has created a real pickle for many investors. While dumping stocks may stop the bleeding, it can also prevent potential gains.

We’ve watched earnings take a nosedive throughout this year’s earnings season. International stocks’ P/E ratios, represented by the MSCI EAFE Index in the chart below have dropped substantially, well below their long-term average. The question is how much lower do they need to fall before we reach the bottom or recession?

Charles Schwab How Much Lower Until The Bottom Chart?

Charles Schwab How Much Lower Until The Bottom Chart? (Charles Schwab)

The S&P 500 has come back from every one of its prior bear markets to rise to another all-time high eventually. The down decade for the stock market following the 2000 dot-com bubble bursting was a notoriously brutal stretch, but stocks have often been able to regain their highs within a few years. My point is that inflation is so high that if you sit on cash too long, you’re intentionally losing 9% and then losing any potential upside. It’s a recipe for disaster long-term and in the words of billionaire Ray Dalio, “Cash is Trash And Equities Are Even Trashier!” Citing high inflation as a guaranteed loser with equities also likely to struggle, Dalio indicates that navigating the current environment is key. Remember your long-term investment objectives, regardless of the market cycle. As such, your investment objectives drive your corresponding risk. While some asset managers may recommend going into the sideline into cash, you cannot consistently time the market, waiting for the opportune time to buy. It’s about time in the market, not timing the market.

Given that expected increasing market volatility should continue, a prudent allocation change may be to increase the amount of cash you hold, but only so much as to not disrupt your risk/return profile. For example, investors may take a 60/40 stock/bond portfolio and allocate a portion to cash, allowing for reduced market portfolio volatility while leaving some powder on the sidelines to capitalize on opportunities like ‘real-return asset’ picks as they present themselves, which maintains one’s long-term risk/return profile. Alternatively, some investors may choose to allocate their cash back to stocks when the Federal Reserve has indicated they will no longer tighten monetary policy or whenever the market has big pullbacks. At the end of the day, the best days in the market tend to follow the worst.

Having no exposure typically is a recipe for disaster and a missed opportunity. One would be wise to focus on quality stocks during times of recession; it goes beyond value and dividend production. Focus on strong balance sheets, low debt levels, strong free cash flow, prudent management, and overall fundamentals. The hope is that the traditional relationship on returns with market volatility spiking and yields falling is that investors find safe havens in bonds that will reduce portfolio volatility. Patience is key.

With the anticipation of a recession and mounting rumors of more rate increases by year-end, investors have options to consider and how best to respond to periods of downturn.

What To Do with Your Investments During a Recession

Don’t be fooled by bear market rallies. They’re often fool’s gold. Last week was the best week since November 2020 across the board, and you saw multiple rallies, as evidenced in the chart below.

May 23 – May 27 SPY Bear Market Rally? (Seeking Alpha)

Though all of the risks that existed before last week still exist today, until we see some clarity and development to bring resolution to the uncertainty of whether a peak in inflation to include the Personal Consumption Expenditure (PCE) index, which increased by 6.3% in April from one year ago; resolution for the war in Ukraine; stability in the supply chain; solidity in the Chinese economy and their ability to fight off COVID-induced shutdowns; it’s essential to stick to your long-term investment objectives. There is nothing you can do to change the stock market or the economy’s reaction. But there are many sectors and investments you can consider to aid you in your investment goals. Consider our investment ideas that may help recession-proof your portfolio.

Top Recession-Proof Investment Ideas

Staples are a defensive sector with a strong likelihood and probability of success of pushing increasing costs to consumers without a significant drop-off in sales and revenues. YTD, the Consumer Staples (XLP) sector is down only 3.42%. Because they are necessities – bare essentials – including food and beverages, personal hygiene, and cleaning products, unlike the Consumer Discretionary Sector (XLY), which has been getting crushed and experienced a 26% decline YTD, consumer staples should experience the least impact on margins and profitability, which is why we have four top stocks to invest in during a bear market or recession.

1. Adecoagro S.A. (NYSE:AGRO)

- Market Capitalization: $1.23B

- Quant Rating: Strong Buy

- Quant Sector Ranking (as of 5/31): 1 out of 177

- Quant Industry Ranking (as of 5/31): 1 out of 55

South American agro-industrial company Adecoagro S.A. (AGRO) plants, harvests, and packages farming crops, foods, and other agricultural products. On a longer-term uptrend, this consumer staple is currently ranked #1 in its sector and industry and possesses A+ momentum.

AGRO Momentum Grade (Seeking Alpha Premium)

AGRO substantially outperforms its quarterly price performance compared to its sector peers. Year-to-date, the stock is +43%, and with agriculture and food in high demand and the natural resources industry growing, this stock continues to trade near its one-year high.

AGRO Valuation

In addition to stellar momentum, AGRO comes at a great discount. Possessing an A- overall valuation grade, the stock not only maintains a 9.12x forward P/E, a near -50% difference to the sector, but the company also has an A+ 0.05x PEG (TTM) ratio, -90% difference to the sector, an indication this stock is hugely undervalued. Trading at $11.14 per share, this is an excellent investment in consumer staples that, in addition to a great price point, captures the rise in agricultural commodity prices.

AGRO Valuation Grade (Seeking Alpha Premium)

As AGRO’s overall metrics have seen improvements over the last few years, you can also see that EPS figures have improved with growth and profitability. Despite some setbacks during the pandemic, AGRO CEO Mariano Bosch noted:

During the past 5 years, we have invested approximately $400 million across all our businesses, in projects that are generating ROICs of over 25%. These investments have improved the efficiency and sustainability of our operations, enhanced our competitive advantages, and allowed us to be better positioned to face all different scenarios.

Let us dive into AGRO’s most recent growth and profitability.

AGRO Growth

In addition to stellar financial performance that resulted in the company approving a $0.32 per share dividend for a total cash distribution of $35 million over two installments, Adecoagro S.A. has experienced tremendous growth over the last year, as evidenced by the below growth grades.

AGRO Growth Grade (Seeking Alpha Premium)

Despite lower rainfall during the first three months of the year that resulted in yields down year-over-year related to areas harvested with little growth potential, March and April saw an uptick that favored AGRO’s sugarcane business and AGRO’s Green Revolution focused on ethanol production, which is capturing the rising prices offering greater potential to grow. Compared to last year’s $18.21M, AGRO reported net income of $63.26M. Revenue of $206.36M was up 18.06% year-over-year.

As a result of increasing prices, AGRO was able to make more use of its fixed assets and inventories, increasing ethanol sales to $57M, a 31.1% increase YoY, and increasing sugar prices. AGRO has excellent current EBIT margins at 21.49% as well as net income margins at 15.20%. With cash from operations remaining solid, we believe this company will continue to capitalize on the tailwinds supported by high commodity prices and it’s clear analysts believe this stock is a strong buy, given the three FY1 Up revisions in the last 90 days.

2. Cal-Maine Foods, Inc. (NASDAQ:CALM)

- Market Capitalization: $2.36B

- Quant Rating: Strong Buy

- Quant Sector Ranking (as of 5/31): 2 out of 177

- Quant Industry Ranking (as of 5/31): 2 out of 55

Together with its subsidiaries, Cal-Maine Foods (CALM) produces, grades, and supplies shell eggs for popular brands like Egg-Land’s Best and Land O’Lakes eggs throughout the U.S. Despite its C+ valuation and less than stellar underlying valuation metrics, this stock’s other collective characteristics including growth, momentum, and revisions are solid, making this stock an egg-cellent pick!

CALM Momentum

CALM Momentum Grade (Seeking Alpha Premium)

On a bullish trend over the last year, +26% YTD and +32% over one year, as evidenced by the above momentum grade, CALM substantially outperforms the sector on a quarterly basis. Because inflation is weighing on earnings power, stocks like CALM are able to pass off increasing costs, including feed, packaging, and delivery costs to consumers. CPI jumped to 8.3% in April, and I was recently stunned at the grocery store, with eggs having some of the highest inflation markups over 10%, with some areas like Florida, seeing as high as 161%, and CALM experiencing a 29.4% increase in its average selling price. While these increases hit consumers’ pockets, continued demand for this staple is allowing CALM to maintain its #1 shell egg producer and distributor position, capturing 19% of the market share; thus, this stock should continue to see growth and profits.

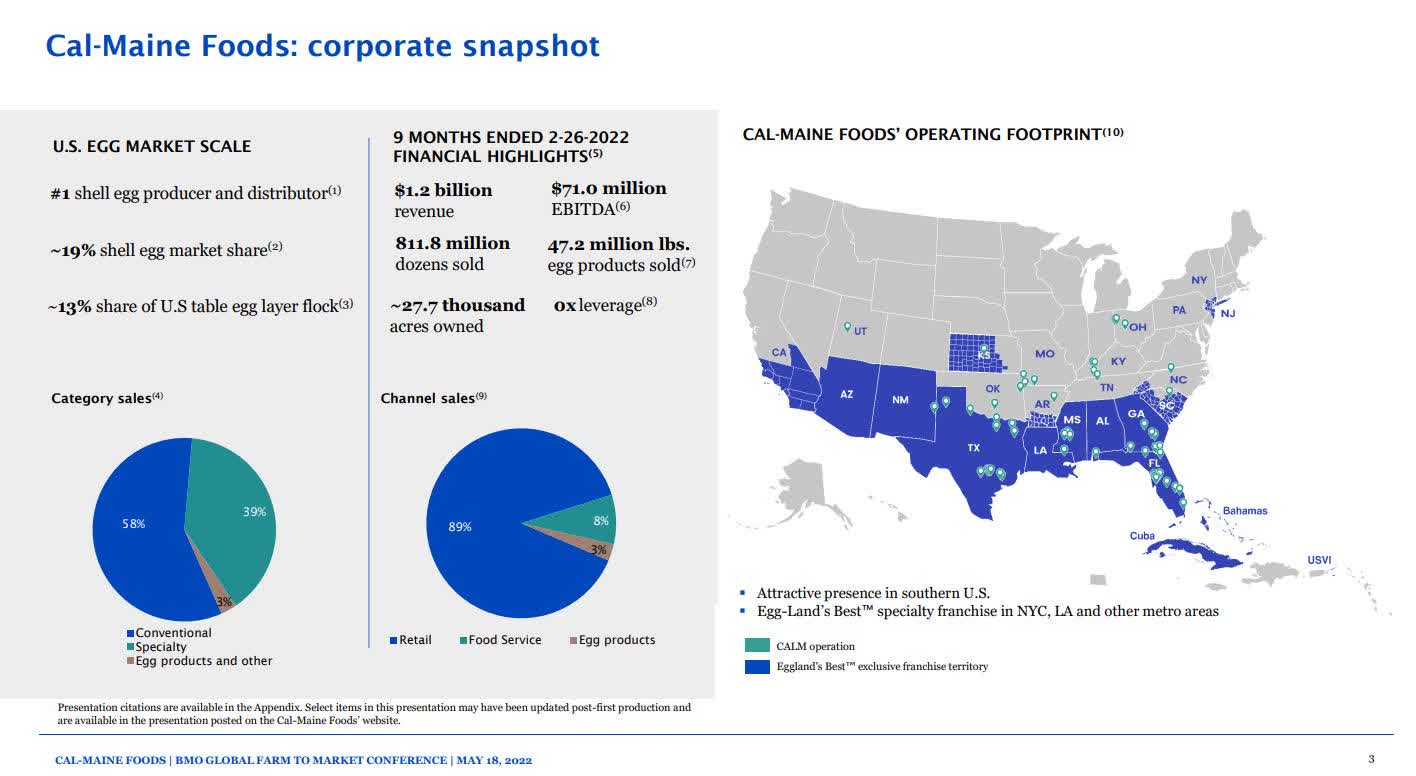

Cal-Maine Corporate Snapshot (Cal-Maine Investor Presentation)

CALM Growth

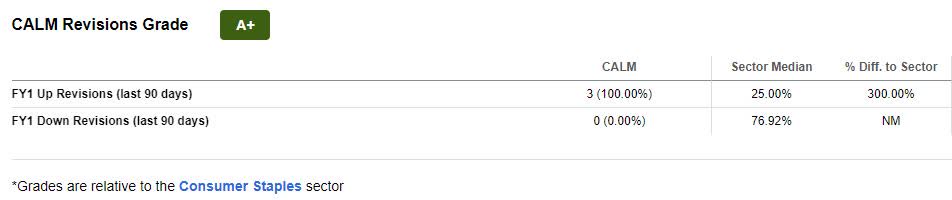

Over the last year, CALM has beaten EPS and revenue estimates 75% of the time. Despite a Q3 2022 EPS of $0.81 missing by $0.01, revenue of $477.49M beat by $9.72M resulting in an A+ Revisions grade and three analysts’ FY1 Up revisions, the company’s net sales were tremendous, an increase of nearly 33%.

CALM Revisions Grade (Seeking Alpha Premium)

Dolph Baker, Chairman & CEO of Cal-Maine Foods stated:

We are pleased to report a strong performance for the third quarter of fiscal 2022. Net sales of $477.5 million represented a third-quarter revenue record, driven by improved shell egg pricing. The net average selling price for all eggs increased 29.4 percent to $1.612 per dozen compared with $1.246 per dozen in the prior-year period…Our fiscal third-quarter gross margin of 19.2 percent improved approximately 600 basis points compared to the prior-year quarter. This increase reflects overall improved market conditions, strong growth in our specialty egg sales, our continued focus on expense management, and our ability to leverage our owned production capabilities.

With tremendous growth metrics and tailwinds that allow this company to capitalize on price markups, coupled with a forward dividend yield of 1.04% and A+ dividend safety grade, this stock is a strong buy and declared a $0.125/share quarterly dividend. Despite inflation taking a toll on many stocks, including in the food sector, eggs are a popular necessity, produced in high volumes, and customers should consider taking a bite out of this stock, as well as our third pick.

3. Pilgrim’s Pride Corporation (NASDAQ:PPC)

- Market Capitalization: $8.07B

- Quant Rating: Strong Buy

- Quant Sector Ranking (as of 5/31): 5 out of 177

- Quant Industry Ranking (as of 5/31): 4 out of 55

Meat packaging and food company Pilgrim’s Pride Corporation (PPC) markets and distributes fresh and frozen chicken, pork, and other meat products internationally. With stellar overall factor grades, this stock is primed for growth and comes at a great value.

PPC Factor Grades (Seeking Alpha Premium)

PPC Valuation & Momentum

Possessing an overall B- valuation grade, Pilgrim’s Pride has a forward P/E ratio of 9.64x, more than 46% below its sector average. In addition, its forward PEG of 0.65x is -73.91% difference to the sector, and stellar forward EV/Sales of 0.65x indicate this stock is severely undervalued, particularly as it continues its bullish trend, +18% YTD in share price.

PPC Momentum Grade (Seeking Alpha Premium)

PPC’s momentum showcases strong price performance, beating sector median peers by more than two- and three-time over its six and nine-month price performance. Like the tailwinds affecting other food stocks, PPC is benefiting from strong demand and elevated meat prices being passed on to consumers. With the company being the second-largest producer throughout the nations it operates, increasing demand for chicken versus red meat has increased PPC’s demand, as more people are switching to poultry, a benefit for growth and profitability figures.

PPC Growth and Profitability

Since 2021, Pilgrim’s Pride has experienced significant growth and higher selling price on the heels of people switching to a new chicken breed as well as from red meats. With a 22% price increase in 2021, the company anticipates future price increases as a result of inflation, driving sales growth. Q1 EPS of $1.18 beat by $0.50 and revenue of $4.24B beat by $141.73M, a near 30% increase year-over-year.

PPC Growth Grade (Seeking Alpha Premium)

Along with stellar growth, PPC diversified its geographic reach and improved its e-commerce, sales, and margins. Q1 2022 prepared food sales saw a jump of 35% compared to last year.

Adjusted EBITDA margins in Q1 were 15.9% in the U.S. compared to 6.5% a year ago…Adjusted EBITDA in the U.S. for Q1 came in $412 million compared to $131 million a year ago. Both gross and operating margins were higher compared to 2021 due to higher commodity market pricing, strong consumer demand, improved operational efficiencies, and growth with our key customers. – Matt Galvanoni, Pilgrim’s Pride CFO.

Given the market outlook and persisting inflationary concerns, higher commodity prices and persistent demand should bode very well for PPC’s outlook, as these trends should continue throughout the year.

4. Hostess Brands, Inc. (NASDAQ:TWNK)

- Market Capitalization: $2.97B

- Quant Rating: Strong Buy

- Quant Sector Ranking (as of 5/31): 7 out of 177

- Quant Industry Ranking (as of 5/31): 6 out of 55

Popular packaged food maker known for Twinkies, Ding Dongs, and Ho Hos, Hostess Brands, Inc. (TWNK) develops, manufactures, and distributes snacks around the globe. Full disclosure, I used to love Twinkies and Ding Dongs. If you’re looking for a company to invest in during a downturn or recession, not only does Hostess possess the fundamentals, I’m unsure of the ingredients in their snack cakes, but their extended shelf life can probably survive an apocalypse! And for sure, their prices can fit even a recessionary budget.

TWNK Valuation Grade (Seeking Alpha Premium)

TWNK comes at a fair valuation and price point near its sector median peers. Although the stock is trading slightly above its peers with a forward P/E ratio of 21.95x, the stock has been trending up, with a one-year price increase of +32%. Direct-to-warehouse strategizing has allowed the company to gain market share via its extended shelf-life technology and pre-built displays that offer more visibility for impulse buys during checkout, and the company has also been able to focus on cutting costs, ideal for growth and profitability.

TWNK Growth & Profitability

Hostess has been able to stand the test of time. A 100-year-old brand, this stock consistently showcases tremendous growth, most recently reporting 25% organic sales growth for Q1 2022, prompted by a 15% increase in volume, and the launch of new products and innovations in Baby Bundts, caffeinated donuts, and other products.

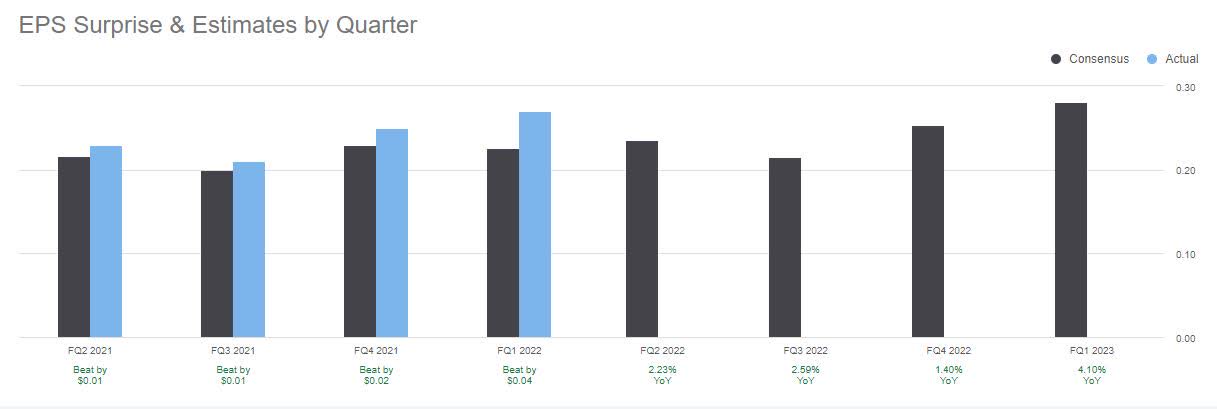

TWNK EPS Estimates (Seeking Alpha Premium)

TWNK delivered tremendous Q1 2022 results, with an EPS of $0.27 beating by $0.04 and revenue of $332.05M beating by $33.06M, its ninth consecutive quarter of 9% sales growth and the highest sales growth in the company’s history.

Higher volumes accounted for nearly 15% points of our quarterly sales growth, reflecting strong innovation and consumer demand, as well as the continued excellence of our supply chain, as we execute well in a dynamic environment…Over the next few years, we expect to deliver mid-single-digit organic revenue growth, 5% to 7% EBITDA growth, and 7% to 9% EPS growth that we believe will establish us as a best-in-class snacking company that generates top-tier total shareholder returns. – Andrew Callahan, Hostess President & CEO.

Hostess’s strong appetite for acquisitions has proven fruitful, bolstering sales, allowing it to outlast varying nutritional and diet fads brought about by competitors, as well as has established a lucrative business in the breakfast and cookie segments. Despite the healthy and clean eating trends, Hostess has stayed the course and as the second-largest brand next to Little Debbie, we believe this stock like the snack cakes is here to stay. Consider adding TWNK to your portfolio.

s.