The year 2022 is on track to be remembered for its historic market volatility. While the S&P 500 (SPY) had its worst start in decades, the Nasdaq had its worst start ever.

The sell-off initially affected small and mid-caps. However, it has now extended to the “generals,” with Apple (AAPL), Amazon (AMZN), Alphabet (GOOG), and Microsoft (MSFT) all trading significantly down from their previous high.

The past six months have been catastrophic for many categories, particularly those that benefited from pandemic tailwinds. There is no place to hide if you invest in fast-growing companies. Let’s use benchmarks to see how far they are off their previous peak:

- Fintech (FINX): -51%.

- E-commerce (EBIZ): -50%.

- Cloud computing (WCLD): -51%.

- Ad-tech and mar-tech (MRAD): -48%.

Many individual stocks in these categories have been cut in half or more, making the recent sell-off far worse than March 2020.

And it’s not just mean reversion after a COVID “round-trip.” These ETFs have been underperforming the S&P 500 since their pre-COVID inception.

The near-term outlook is dominated by bearish sentiment. According to the American Association of Individual Investors, only 20% of investors are bullish. However, this can be a contrarian indicator. After all, great entry points are found in bear markets.

Investor Sentiment Survey (AAII)

While I expect doom and gloom predictions in the comment section of this article, investors tend to overlook that things could also turn out better than expected in the coming quarters.

Many factors are at play: the end of the pandemic-era stimulus, inflation fear, potential interest rate hikes, the Russian invasion of Ukraine impacting commodity prices, and an expected recession.

It can be tempting to run for the hills in a challenging environment.

I say au contraire, my friend!

Historically, when the market suffers such a pullback, it creates opportunistic entry points to accumulate shares of high-quality companies that fall in unison with the rest of their industry. The main challenge? It requires holding your nose and accepting that you can’t time the bottom.

As explained in my previous article about the 4 Simple Rules to protect your portfolio, I’m not trying to be a hero. Instead, I steadily ease my way into the market. I’m a net buyer of stock every month, rain or shine, setting aside a portion of my income to buy shares of outstanding businesses. I expect this strategy to do wonders over a lifetime of investing.

My approach has been the same through the ups and downs of the market over the years:

- Buy great businesses diligently.

- Hold on to them tenaciously.

These pullbacks are usually moments to seize, not to fear. Sell-offs like this one have been the source of my best trades.

Fundamentals drive stock performance over a multi-year time horizon. The value of a business depends on the profit it can return to its shareholder. That profit results from business operations, with revenue growth and margin expansion.

Focusing on high-quality businesses

Today, I’m focusing on three businesses that have been massive winners since becoming public.

- MercadoLibre (NASDAQ:MELI) has been a 27-bagger since its 2007 IPO.

- CrowdStrike (NASDAQ:CRWD) has been a 3-bagger since its 2019 IPO.

- The Trade Desk (NASDAQ:TTD) has been a 17-bagger since its 2016 IPO.

They have essentially been cut in half. And, believe it or not, these returns are after factoring in the massive pullback in recent months.

Such pullbacks are a rarity. Once or twice every decade.

Could these stocks fall another 50% in the coming months? Absolutely! Unfortunately, that’s a reality we have to live with when we invest in stocks.

While they could fall further in the near term, they have rarely looked this attractive if you invest with a multi-year time horizon.

Here’s why I find them compelling today:

MercadoLibre

MercadoLibre Logo (Company Website)

Argentina-based MercadoLibre has been a long-time winner of the App Economy Portfolio (my real-money portfolio).

There is a ton to love about this leader in Latam at the crossroads of e-commerce and fintech.

The company has seen an incredible revenue growth acceleration with a three-digit growth throughout COVID. And in Q1 FY22, it continued to grow very fast despite very challenging comps.

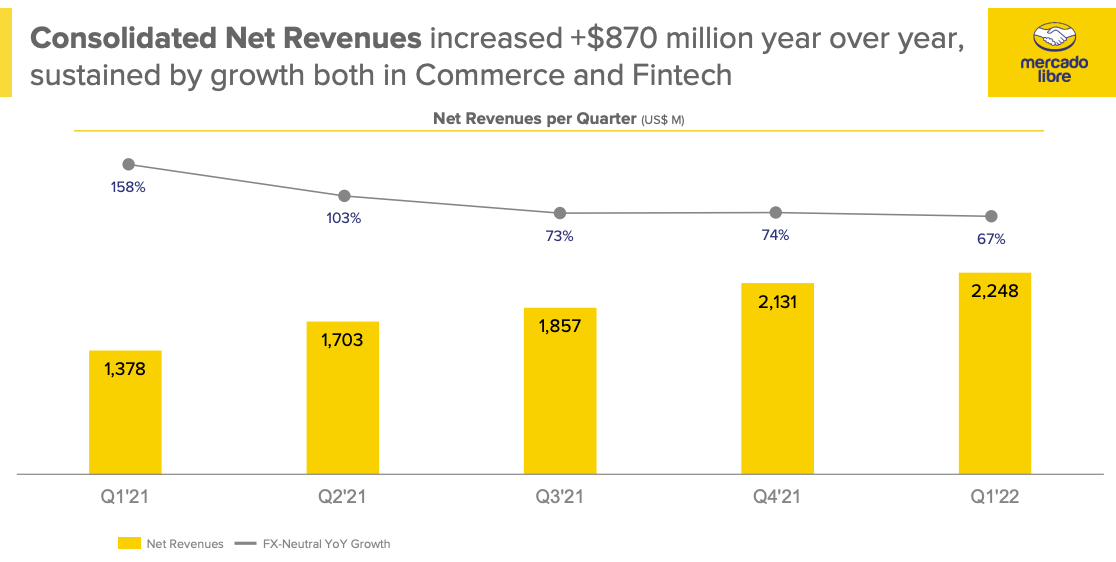

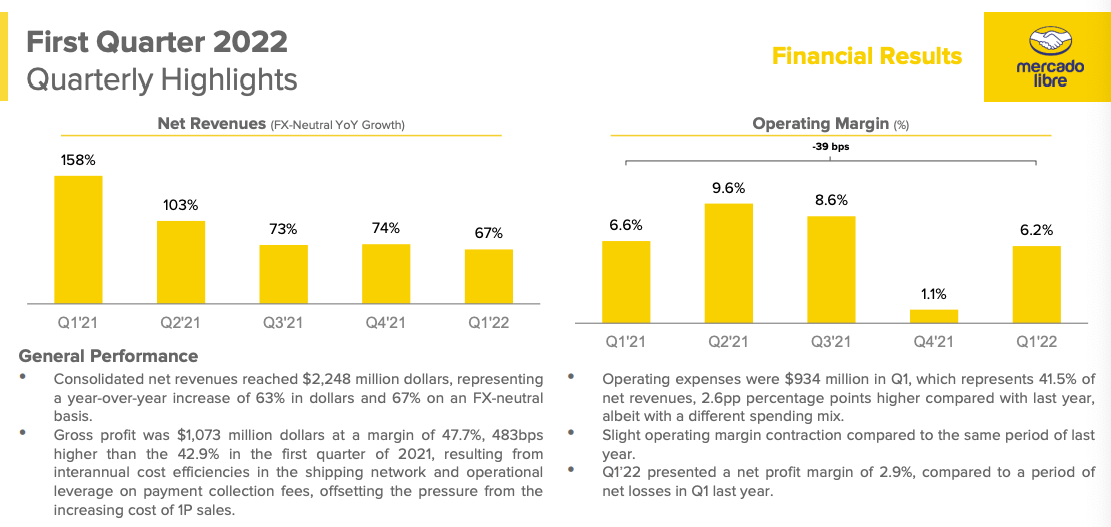

Revenue reached $2.25B in Q1 FY22 (+67% Y/Y), compared to Q1 FY21, which already saw revenue grow +158% Y/Y.

MercadoLibre Revenue (Q1 FY22 Earnings Slides)

MercadoLibre is another big winner of the accelerated transition to digital payment and e-commerce in its corner of the world.

What I like about the company is its optionality. You could call MELI the Amazon (retail side) and Square/PayPal of South America. Morgan Stanley pointed out that the company was “on the path to be a one-stop fintech provider.”

The company has the reach (81 million active users) and the potential to expand into other fintech solutions (digital wallet, insurance, asset management solutions, and so on).

Other contenders are vying for a share of the market as well. Among them are Sea Limited (SE), Amazon (AMZN), and Alibaba (BABA). But given the market size (more than 400 million people), multiple winners can emerge.

The company breaks down its performance in four main businesses:

- Marketplace – Mercado Libre.

- Logistics – Mercado Envios.

- Payments – Mercado Pago.

- Credits – Mercado Credito.

In Q1 FY22, the revenue breakdown was:

- Commerce: $1.3B or 57% of revenue (+44% Y/Y).

- Fintech: $1.0B or 43% of revenue (+113% Y/Y).

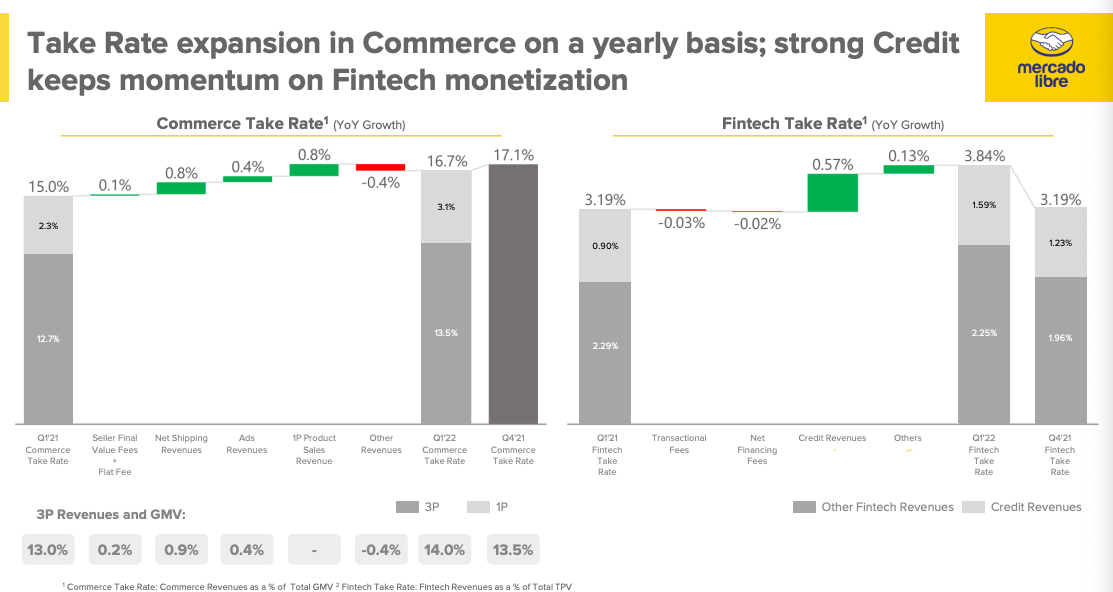

Fintech represents a growing part of the business. The take rate has improved Y/Y for both segments: 16.7% for Commerce (+1.7pp Y/Y) and 3.84% for Fintech (+0.65pp Y/Y).

MercadoLibre Take rate (Q1 FY22 Earnings Slides)

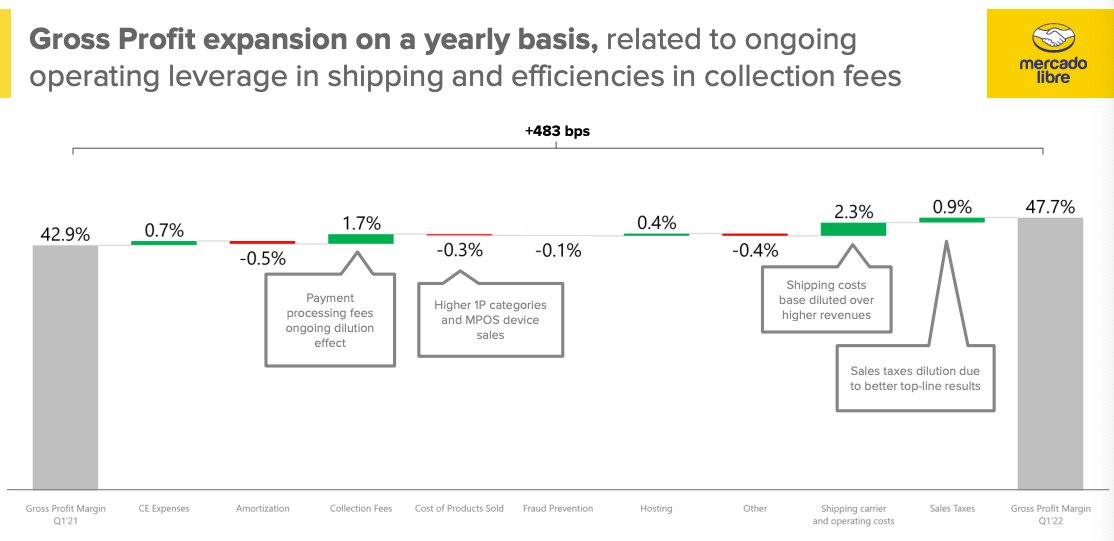

MELI has improved its gross margin to 47.7% (+4.8pp Y/Y) due to scalability with higher revenue.

MercadoLibre Gross Margin (Q1 FY22 Earnings Slides)

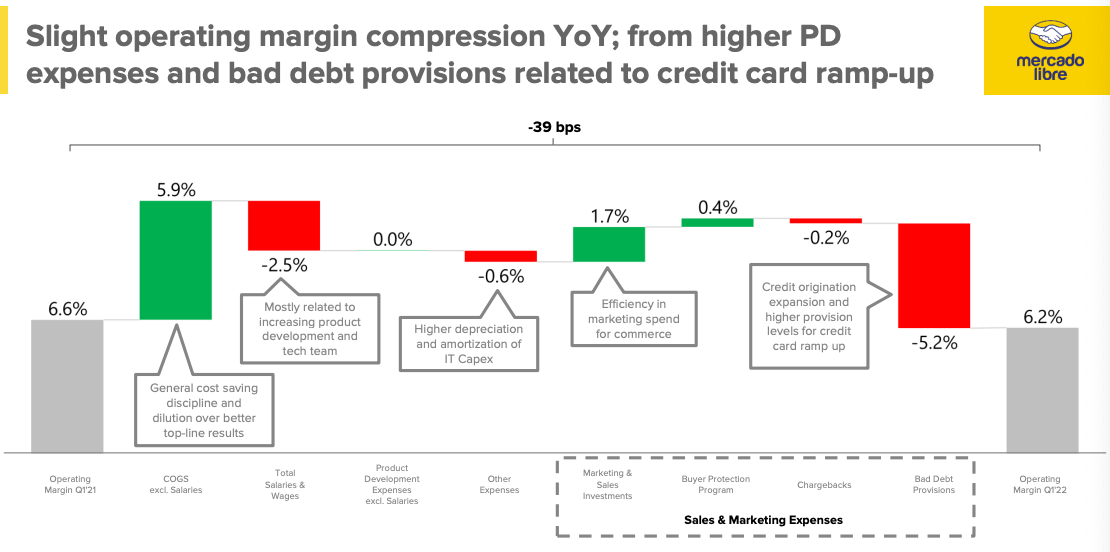

The EBIT margin was slightly down to 6.2% (-0.4pp Y/Y), with cost efficiencies offset by bad debt provisions. The company has maintained its profitability while growing at a breakneck pace.

MercadoLibre Operating Margin (Q1 FY22 Earnings Slides)

The risk/reward profile of the company is becoming more attractive.

- Opportunities:

- Over time, the company’s take rate improvement illustrates its pricing power and indicates a durable economic advantage.

- MELI’s reach allows for new revenue streams over time. The company keeps expanding its TAM by entering new categories, in a way reminiscent of Block (SQ) or Amazon (AMZN). Fintech could become the leading segment in the quarters ahead and lead to re-accelerating growth.

- Aristotle taught us that “the whole is greater than the sum of the parts,” and MELI could be a perfect example. The success of each segment can fuel the others, with potential for user acquisition, retention, and monetization across platforms.

- Risks:

- E-commerce and fintech are volatile to the macro-environment and could struggle in the quarters ahead. In addition, Brazil just exited a recession in the fourth quarter of 2021.

- Weak economic growth and high inflation in South America could challenge MELI in the near term.

- Non-performing loans as a percentage of the portfolio increased from 24.2% to 27.6%, similar to Q2 and Q3 FY21. It will be necessary to watch if management can keep it under control in worsening market conditions.

Q1 FY22 Highlights:

MercadoLibre Q1 Highlights (Q1 Earnings Slides)

Note: GMV = Gross Merchandise Volume. TPV = Total Payment Volume

- GMV grew +32% Y/Y to $7.7B (+32% Y/Y in Q4) fx neutral.

- TPV grew +72% to $25B (vs. +73% Y/Y in Q4) fx neutral.

- Unique active users grew +16% Y/Y to 81 million (vs. +11% Y/Y in Q4).

- Net Revenues grew +67% Y/Y to $2.2B, (vs. +74% in Q4) fx neutral.

- Gross Margin was 48% (+5pp Y/Y).

- Operating margin was 6% (-1pp Y/Y).

- Operating cash flow margin was -10% (+9pp Y/Y).

- Cash and short-term investments on its balance sheet were $3B.

The company’s balance sheet is not as robust as other App Economic Portfolio companies, with $3B of long-term debt. However, since MELI generated more than $1.0B in cash from operations in the past 12 months, it’s not an area of concern for me.

On a GAAP basis:

- Gross margin has rebounded to 48%.

- Sales & Marketing costs are going down steadily, at 24%.

- Operating margin is trending back up, at 6%.

The company’s most recent financial results for Q1 FY22 can be summarized as follows:

- Extreme top-line growth (+67%) – showing strength.

- Stable gross margin at 48% – showing long-term potential.

- Stable sales & marketing costs at 24% – showing scalability.

- Operating margin staying positive during this fast-growth phase.

- Positive cash from operations in the past year – showing sustainability.

While its margin profile has worsened, MELI has more than quadrupled its revenue in the past three years.

Why is this opportunity timely?

For one thing, MELI is rarely trading more than 40% down from its previous high. It happened only a few times in the past decade, in 2014, 2015, and 2016.

The company is trading at its lowest revenue multiple since the bottom of the Great Recession in 2009.

With a $41B enterprise value, MELI is trading at about 41 times trailing operating cash flow, which appears undervalued given its growth profile and potential for future margin expansion.

The company has received many awards and accolades across several platforms (such as Great Place to Work and Top Of Mind) and is one of the best rated on Glassdoor.