Household final consumption expenditure, in real terms, grew by 6.10% and 16.59% in Q3 and Q4 2020, respectively, on a year on year basis, compared to the -1.98% growth in Q3 2019 and -0.41% growth in Q4 2019.

Overall, in 2020, real household final consumption expenditure rose by 0.81% from -1.06% recorded in 2019. On a quarter on quarter basis, real household consumption expenditure grew by 38.85% in Q3 and 20.76% in Q4 2020.

In Q3 2020, the gross domestic product declined in real terms by -3.62% year-on-year but rose to 0.11% in Q4 2020, ending the trend of two-quarters of negative growth. For annual 2020, the gross domestic product grew in real terms by -1.92% year-on-year, slower than 2.27% recorded in 2019, and 1.91% recorded in 2018.

In nominal terms, household final consumption expenditure grew by -1.83% in Q3, and -0.71% in Q4 2020, resulting in an annual growth rate of -1.48%. The annual growth rate was -11.33% points slower than recorded in the previous year.

On a quarter on quarter basis, growth was recorded at 23.04% in Q3, and 7.68% in Q4 2020, compared to the preceding year’s 11.74%, and 6.46% in the corresponding quarters. Household consumption accounted for 63.63% of real GDP at market prices in Q3 2020, and even higher at 70.45% in Q4 2020.

| Growth in Consumption Components, 2019, 2020 (Real), Percent,%) |

|

|

|

2019 |

|

|

|

2020 |

|

|

|

| |

Q1 |

Q2 |

Q3 |

Q4 |

Q1 |

Q2 |

Q3 |

Q4 |

| YoY |

|

|

|

|

|

|

|

|

| Households |

-2.68 |

0.75 |

-1.98 |

-0.41 |

-4.86 |

-18.11 |

6.10 |

16.59 |

| NPISH |

-3.25 |

7.84 |

53.77 |

7.92 |

-0.38 |

174.87 |

289.76 |

418.54 |

| Government |

8.88 |

0.14 |

2.26 |

22.38 |

6.80 |

148.29 |

99.18 |

12.13 |

| Individual |

-41.59 |

-28.86 |

-33.32 |

-19.61 |

-1.81 |

158.30 |

106.49 |

15.75 |

| Collective |

52.31 |

15.70 |

24.09 |

47.85 |

9.65 |

144.99 |

96.78 |

10.93 |

|

2019 |

|

|

|

2020 |

|

|

|

| Q on Q |

Q1 |

Q2 |

Q3 |

Q4 |

Q1 |

Q2 |

Q3 |

Q4 |

| Households |

-20.47 |

6.33 |

7.18 |

9.89 |

-24.03 |

-8.48 |

38.85 |

20.76 |

| NPISH |

23.68 |

-56.40 |

45.71 |

37.37 |

14.17 |

20.29 |

106.61 |

82.75 |

| Government |

-4.04 |

-5.84 |

2.19 |

32.54 |

-16.26 |

118.90 |

-18.02 |

-25.39 |

| Individual |

-36.96 |

-5.85 |

2.15 |

32.58 |

-22.99 |

147.68 |

-18.34 |

-25.68 |

| Collective |

15.92 |

-5.84 |

2.20 |

32.53 |

-14.03 |

110.40 |

-17.91 |

-25.29 |

| Growth in Consumption Components, 2019, 2020 (Nominal), Percent,%) |

|

|

2019 |

|

|

|

2020 |

|

|

|

| |

Q1 |

Q2 |

Q3 |

Q4 |

Q1 |

Q2 |

Q3 |

Q4 |

| YoY |

|

|

|

|

|

|

|

|

| Households |

7.37 |

15.00 |

7.37 |

10.07 |

8.15 |

-10.84 |

-1.83 |

-0.71 |

| NPISH |

0.55 |

11.38 |

57.80 |

10.75 |

2.23 |

180.28 |

167.64 |

12.18 |

| Government |

13.17 |

3.43 |

4.94 |

25.59 |

9.61 |

153.17 |

104.41 |

15.07 |

| Individual |

13.20 |

3.45 |

4.92 |

25.60 |

5.19 |

163.38 |

111.91 |

18.79 |

| Collective |

13.16 |

3.43 |

4.95 |

25.59 |

11.06 |

149.81 |

101.94 |

13.84 |

|

2019 |

|

|

|

2020 |

|

|

|

| Q on Q |

Q1 |

Q2 |

Q3 |

Q4 |

Q1 |

Q2 |

Q3 |

Q4 |

| Households |

-15.14 |

9.03 |

11.74 |

6.46 |

-16.61 |

-10.12 |

23.04 |

7.68 |

| NPISH |

24.48 |

-55.84 |

45.71 |

38.26 |

14.91 |

21.07 |

39.14 |

-42.05 |

| Government |

-3.42 |

-4.62 |

2.19 |

33.40 |

-15.71 |

120.32 |

-17.49 |

-24.90 |

| Individual |

-3.39 |

-4.62 |

2.15 |

33.44 |

-19.10 |

138.81 |

-17.81 |

-25.20 |

| Collective |

-3.43 |

-4.61 |

2.21 |

33.39 |

-14.60 |

114.55 |

-17.38 |

-24.80 |

Not-for-Profit-Institutions-Serving-Households (NPISH) Consumption

Final consumption expenditure by non-profit institutions serving households recorded growth rates of 289.76% in Q3 and 418.54% in Q4 2020, year on year in real terms. For annual 2020, growth in real expenditure for this component was recorded at 212.36% year on year. Quarter on quarter, growth in real NPISH expenditure stood at 106.61% in Q3 but dropped to 82.75% in Q4 2020. This expenditure component accounted for 1.30% of real GDP expenditure at market price in Q3 and a share of 2.19% in Q4 2020. For 2020, it accounted for 1.24% of total real GDP expenditure at market prices.

General Government

In Q3 and Q4 2020, real general government expenditure grew by 99.18% and 12.13% respectively, compared to 2.26% and 22.38% in 2019. On an annual basis, real growth for general government expenditure in 2020 stood at 61.58% compared to 8.78% in 2019. Quarter on quarter, growth was recorded at -18.02% and -25.39% in Q3 and Q4 2020 respectively.

In nominal terms, government expenditure grew by 104.41% in Q3 and 15.07% in Q4 2020 resulting in an annual nominal growth rate of 65.52% in 2020. Government expenditure, however, grew more rapidly in 2020 than in 2019 by 53.35% points. In 2020, this component accounted for 9.40% of total real GDP expenditure at market price.

Gross Fixed Capital Formation (GFCF)

Real GFCF recorded growth in the third and fourth quarters of 2020 at -6.57% and -1.08% year-on-year respectively. On an annual basis, real GFCF grew by -7.55%, or by -15.84% points lower than in 2019.

Quarter on quarter, real GFCF grew by 3.25% and 22.83% in Q3 and Q4 2020 respectively. In nominal terms, Q3 and Q4 2020 recorded 21.78% and 36.42% growth rates. GFCF grew by 23.21% nominally in 2020 while accounting for 14.95% of total real GDP expenditure at market prices in 2020.

Changes in Inventories

Changes in inventories, often regarded as a sign of economic confidence (as firms stock up on products if they anticipate higher future demand), declined by -7.76% and -9.01% in Q3 and Q4 2020 respectively in real terms.

For 2020, this component grew by 5.94% compared to a growth of -26.23% in the previous year. In nominal terms, changes in inventories grew by 0.86% year on year in 2020 but account for less than 1% of total real GDP expenditure at market prices.

Consumption of Fixed Capital

Consumption of fixed capital is a measure of depreciation of assets and represents the difference between gross domestic product (GDP) and net domestic product (NDP). Growth in consumption of fixed capital in real terms declined by -0.71% in Q3 2020 and by -0.89% in Q4 2020 compared to -44.78% recorded in Q3 2019 and -0.34% recorded in Q4 2019.

The annual growth rate was -1.29% in 2020, better than -23.15% recorded the previous year. In nominal terms, Q3 and Q4 2020 grew by 6.86% and 13.64% respectively. CFC grew by 7.05% in 2020 compared to 16.33% a year earlier.

| Growth in Capital Accumulation in 2019, 2020 (Real), (percent, %) |

|

|

|

|

2019 |

|

|

|

2020 |

|

|

|

| YoY |

Q1 |

Q2 |

Q3 |

Q4 |

Q1 |

Q2 |

Q3 |

Q4 |

| GFCF |

13.71 |

13.34 |

-0.13 |

6.31 |

4.46 |

-25.38 |

-6.57 |

-1.08 |

| Changes in Inv. |

-9.20 |

-49.25 |

-44.84 |

-0.08 |

-4.18 |

59.31 |

-7.76 |

-9.01 |

| Cons. of fixed capital |

-6.69 |

-42.97 |

-44.78 |

-0.34 |

-2.44 |

-0.73 |

-0.71 |

-0.89 |

|

2019 |

|

|

|

2020 |

|

|

|

| Q on Q |

Q1 |

Q2 |

Q3 |

Q4 |

Q1 |

Q2 |

Q3 |

Q4 |

| GFCF |

-0.14 |

11.17 |

-17.46 |

16.02 |

-1.88 |

-20.58 |

3.35 |

22.83 |

| Changes in Inv. |

6.28 |

-41.82 |

-13.70 |

87.24 |

1.92 |

-3.27 |

-50.04 |

84.71 |

| Cons. Of fixed capital |

-12.71 |

-36.93 |

-11.47 |

104.48 |

-14.55 |

-35.83 |

-11.45 |

104.10 |

| Growth in Capital Accumulation in 2019, 2020 (Nominal), (percent, %) |

|

|

|

2019 |

|

|

|

2020 |

|

|

|

| Y on Y |

Q1 |

Q2 |

Q3 |

Q4 |

Q1 |

Q2 |

Q3 |

Q4 |

| GFCF |

70.89 |

54.07 |

30.21 |

38.13 |

37.64 |

-1.76 |

21.78 |

36.42 |

| Changes in Inv. |

10.74 |

10.13 |

15.05 |

13.02 |

9.87 |

-3.49 |

-6.68 |

4.34 |

| Cons. of fixed capital |

13.80 |

23.77 |

15.16 |

12.73 |

11.87 |

-3.42 |

6.86 |

13.64 |

|

2019 |

|

|

|

2020 |

|

|

|

| Q on Q |

Q1 |

Q2 |

Q3 |

Q4 |

Q1 |

Q2 |

Q3 |

Q4 |

| GFCF |

7.70 |

19.42 |

-8.52 |

17.40 |

7.32 |

-14.77 |

13.41 |

31.51 |

| Changes in Inv. |

8.49 |

13.95 |

-10.58 |

2.24 |

5.47 |

0.10 |

-13.54 |

14.31 |

| Cons. Of fixed capital |

-10.89 |

23.52 |

-8.27 |

11.65 |

-11.57 |

6.64 |

1.50 |

18.73 |

Exports of Goods and Services

In the third and fourth quarters of 2020, real exports grew by -42.05% and -57.79%, year on year, resulting in an annual growth rate of -26.96%, or 41.94% points lower than 14.98% recorded in 2019. Quarter on quarter, however, growth in real exports remained negative from Q1 2020 to Q4 2020.

In nominal terms, exports in goods and services fell by -40.62% in Q3 and -35.96% in Q4 2020 to reach an annual growth rate of -34.24% in 2020 compared with 3.53% in 2019.

Imports of Goods and Services

As with exports, imports of goods and services also declined in real terms, recording -22.74% in Q3 and -39.93% in Q4. On an annual basis, however, the real growth of imports was worse than in 2019, at -23.30% in 2020 compared to 27.26% in the previous year. On a quarter on quarter basis, imports grew by 16.29% in Q3 but declined -3.48% in Q4 2020.

Nominal imports of goods and services fell during the three quarters (Q2, Q3 & Q4 2020), recording -22.23% in Q2, -4.54% in Q3, and -25.54% in Q4 2020, year on year, to give an annual growth rate of -11.38%. This was -38.97% points lower than the annual growth rate of 2019. Quarter on quarter, nominal imports rose in Q3 by 22.16% but declined in Q4 2020 to -3.15 %.

Net Balance of Trade

Due to declining rates of growth in exports and imports in 2020, the growth in the net balance of trade (or net exports) was negative in Q3 and Q4 2020. On a year on year basis, the net trade balance recorded a -52.39% growth rate in real terms in Q3 and a -72.61% growth rate in Q4.

This resulted in an annual growth rate of -29.55% in real terms. On a quarter on quarter basis, the net trade balance grew by -30.43% and -53.90% in Q3 and Q4 2020 respectively. This component accounted for 13.25% of total real GDP expenditure at market prices in 2020.

| Growth in Trade and Services in 2019, 2020 (Real), (percent, %) |

|

|

|

|

2019 |

|

|

|

2020 |

|

|

|

| |

Q1 |

Q2 |

Q3 |

Q4 |

Q1 |

Q2 |

Q3 |

Q4 |

| Y on Y |

|

|

|

|

|

|

|

|

| Exports |

16.84 |

19.61 |

11.01 |

14.10 |

15.49 |

-13.40 |

-42.05 |

-57.79 |

| Imports |

34.13 |

57.71 |

0.02 |

30.37 |

9.08 |

-33.88 |

-22.74 |

-39.93 |

| Trade Balance |

7.08 |

0.00 |

17.94 |

3.40 |

20.02 |

3.22 |

-52.39 |

-72.61 |

|

2019 |

|

|

|

2020 |

|

|

|

| Q on Q |

Q1 |

Q2 |

Q3 |

Q4 |

Q1 |

Q2 |

Q3 |

Q4 |

| Exports |

-4.52 |

-2.10 |

27.85 |

-4.52 |

-3.36 |

-26.59 |

-14.45 |

-30.46 |

| Imports |

-0.32 |

5.85 |

-0.47 |

24.14 |

-16.59 |

-35.84 |

16.29 |

-3.48 |

| Trade Balance |

-7.28 |

-7.73 |

50.84 |

-19.87 |

7.62 |

-20.65 |

-30.43 |

-53.90 |

| Growth in Trade and Services in 2019, 2020 (Nominal), (percent, %) |

|

|

|

|

2019 |

|

|

|

2020 |

|

|

|

| |

Q1 |

Q2 |

Q3 |

Q4 |

Q1 |

Q2 |

Q3 |

Q4 |

| Y on Y |

|

|

|

|

|

|

|

|

| Exports |

-0.76 |

3.42 |

6.44 |

4.84 |

-9.22 |

-49.78 |

-40.62 |

-35.96 |

| Imports |

34.59 |

58.32 |

0.31 |

30.48 |

11.45 |

-22.23 |

-4.54 |

-25.54 |

| Trade Balance |

-1640.97 |

-481.96 |

-20.92 |

105.67 |

74.53 |

51.16 |

163.81 |

-9.97 |

|

2019 |

|

|

|

2020 |

|

|

|

| Q on Q |

Q1 |

Q2 |

Q3 |

Q4 |

Q1 |

Q2 |

Q3 |

Q4 |

| Exports |

0.75 |

2.21 |

12.72 |

-9.68 |

-12.76 |

-43.45 |

33.26 |

-2.59 |

| Imports |

-0.26 |

5.88 |

-0.48 |

24.15 |

-14.81 |

-26.12 |

22.16 |

-3.15 |

| Trade Balance |

-3.23 |

17.08 |

-35.64 |

182.03 |

-17.88 |

1.40 |

12.33 |

-3.75 |

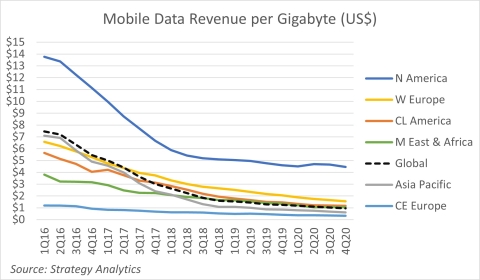

Figure 1. Mobile Data Revenue per Gigabyte in $USD (Source: Strategy Analytics, Inc.)

Figure 1. Mobile Data Revenue per Gigabyte in $USD (Source: Strategy Analytics, Inc.)