Inflation is running hot, there is a great deal of speculation in the markets, and it is a real possibility the Fed waited way too long to raise rates. After announcing late last year, plans to taper asset purchases and tighten monetary policy, the Fed continued buying billions in bonds and assets through March 2022. If the Fed knew it needed to tighten, why were they easing and continuing to purchase assets? This created a lot of uncertainty in the markets.

An exorbitant amount of liquidity has distorted asset prices and risk, hence a balance sheet just under $9T. As Seeking Alpha Contributor Goldmoney writes in Too Much Liquidity:

The Fed sees that there is too much unused liquidity. And making the situation worse, instead of raising money through bond sales, the US Treasury has been drawing down on its balance at the General Account with the Fed – technically putting money into circulation which was not there before.

Keeping the interest rates at zero while continuing to pump stimulus and cash at no cost into the economy inflates asset prices. It’s equivalent to pumping steroids into the free markets. Not only is the excess cash causing asset prices and cost of goods sold (COGS) to run rampant as demand outpaces supply, pumping fiscal stimulus into people’s pockets through Q1 of 2022 exasperates supply-demand issues, perpetuating higher inflation, making it appear that everything the Fed has done post-financial crisis intends to eradicate growth and suffocate both the economy and markets.

The tighter monetary policy is already impacting the economy, the fixed-income markets, and the equity markets. The economy is slowing, which we saw with the first-quarter contraction in GDP, a dramatic drop in new home sales by almost 17% in April, and many companies complaining about margins. The Fed still wants to raise rates by 200-300 basis points before year-end while simultaneously reducing its balance sheet. The running joke is that inflation wasn’t transitory, as Fed Chair Powell claimed, which is now apparent and a problem that requires the Fed to thread the needle for a soft landing to avoid a recession. The burning question among investors and the markets is how much will the Fed raise interest rates? With anticipation mounting and rumors of an aggressive increase of 3 percentage points by year-end, which are the best stocks to buy now during rising interest rates?

Profiting During Interest Rate Hikes

In a 2021 article titled Inflation-Proof Your Portfolio: These 3 Energy Stocks Are Very Bullish, I warned investors about inflation as signs were clear it was bubbling up. Some sectors and industries are better suited for inflation and benefit from rising interest rates. Notably, certain financial stocks can benefit from rising interest rates because of net interest income, increasing margins, and lending at higher rates. By example, insurance companies benefit from higher-yielding investments that bode well for their margins and premium baskets. They can also easily pass along their cost to the end customer. Additionally, energy and commodities have proven to benefit and pass along cost, with prices remaining at all-time highs.

If you’re considering stocks at a reasonable price with solid growth, profitability, and good momentum, we have three top stocks for Fed rate hikes that fit the bill. Energy stocks can easily pass along costs. They can also offer stable dividend yields and strong cash flow. A steady stream of income in this inflationary environment is what investors are looking for.

1. Chevron Corporation (NYSE:CVX)

- Market Capitalization: $329.73B

- Quant Rating: Strong Buy

- Quant Sector Ranking (as of 5/24): 10 out of 244

- Quant Industry Ranking (as of 5/24): 4 out of 19

- Dividend Safety Grade: B-

Chevron Corporation (CVX) has rebounded significantly from pandemic lows, trading at all-time highs. It is rallying as a Top Energy Stock, aided by the recent news of the company’s renewal of its Venezuelan license. Chevron is a diversified growth stock, operating upstream, midstream, and downstream segments. CVX not only has an excellent track record and solid fundamentals, but it also has the strong possibility to climb further on the back of rising fuel costs and continued “pain at the pump”, making this integrated oil giant great for portfolios and an inflation hedge. I think Warren Buffett agrees, given the additional shares of CVX purchased for his company Berkshire, making Chevron the 4th largest equity holding at $25.9B.

Chevron Valuation

Although Chevron possesses a D+ valuation which is not ideal, a number of its underlying valuation metrics are in line with its peer Exxon Mobil (XOM), including the all-important forward P/E ratio of 10.43x, and both forward EV/Sales and EV/EBITDA command Seeking Alpha B- grades on these underlying valuation metrics. Chevron’s other factor grades are great, and while CVX may not be trading at investors’ preferred discounts, we focus on stocks’ collective attributes.

CVX Factor Grades (Seeking Alpha Premium)

The growth, profitability, momentum, and revisions grades above are attractive. Wall Street is pretty keen on the stock as well. Twenty-four analysts revised their revisions up within 90 days, and there have been zero down revisions. Let’s dive into CVX’s profitability, and growth and the tremendous Q1 results showcased below.

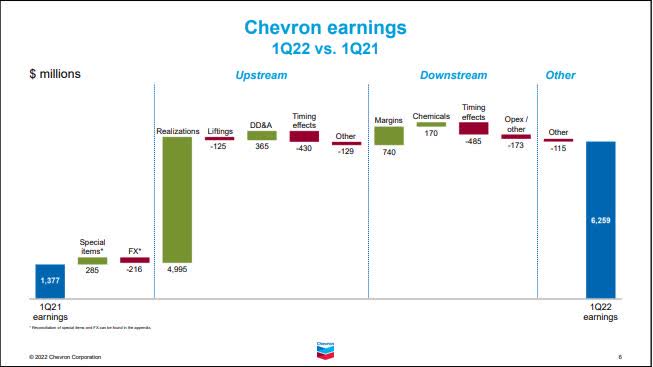

Chevron Q1 2022 Earnings vs Q1 2021 (Chevron Q1 2022 Investor Presentation)

Chevron Profitability & Growth

Large energy companies tend to have the most liquid stocks, best profitability, and the means to pay handsome dividends. Even during market volatility, commodities can be rewarding for protection and profit in an inflationary environment, posing great opportunities amid Fed rate hikes, and why the energy sector is a way to Inflation-Proof A Portfolio. With A+ Cash from Operations sitting at $33.05B and B- EBIT Margins (TTM), ongoing global conflicts continue to drive oil and gas prices, creating a great moat for CVX.

CVX Profitability (Seeking Alpha Premium)

Despite Chevron’s Q1 2022 EPS of $3.36 missing by $0.08, revenues increased by nearly 70%. Chevron adjusted Q1 Earnings were up $4.8B compared to the same period last year, primarily on higher Upstream realizations. Downstream increased due to higher margins. CVX has an excellent balance sheet, which translates into the company’s 34 years of consecutive dividend payments.

We generate more free cash flow than we ever have in the past. And that means we’re able to grow the dividend at very competitive rates and have this buyback that we can maintain across the cycle…We grew our dividend 6% earlier this year. Our dividend is up nearly 20% since COVID, while many in the industry cut their dividends during the last couple of years. Our investment — organic investment is up more than 30% versus last year…With higher commodity prices, affiliate dividends are expected to be $1 billion higher than our previous guidance. – Pierre Breber, Chevron VP & CFO.

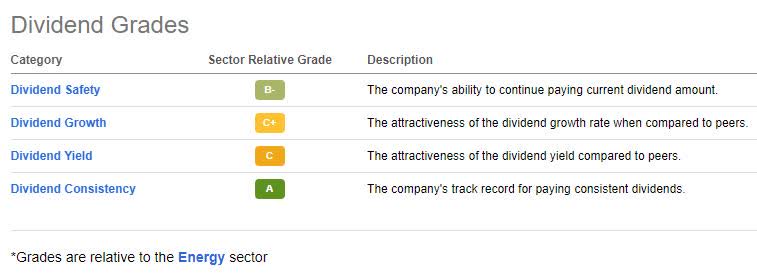

CVX Dividend Grades (Seeking Alpha Premium)

Chevron has a great dividend track record and a strong 3.31% forward dividend yield. As one of the biggest names in oil and gas, Chevron has a consistent track record of supplementing the income being eaten away in this inflationary environment. Given its significant position in the Permian Basin, expansion projects in Kazakhstan, and potential discoveries in Mexico and Brazil, Chevron’s runway looks excellent, with expected free cash flow to increase. We expect Chevron to deliver high returns going forward, expanding margins by capitalizing on high commodity prices, even amid fed rate hikes.

2. The Mosaic Company (NYSE:MOS)

- Market Capitalization: $20.98B

- Quant Rating: Strong Buy

- Quant Sector Ranking (as of 5/24): 8 out of 268

- Quant Industry Ranking (as of 5/24): 3 out of 13

- Dividend Safety Grade: A-

The Mosaic Company (MOS), through its subsidiaries, markets potash, a potassium-rich salt mined from seabeds used in fertilizers to support crop yields and enhance water preservation and phosphate nutrients globally. Fertilizer companies are shattering records to keep up with demand, and Mosaic is a top fertilizer stock to watch. This is a great stock pick for Fed rate hikes because it’s virtually inflation-proof, encompassing food – staples – necessities. As sanctions persist throughout Europe, potash and nitrogen-producing companies like MOS are capitalizing.

Mosaic Valuation

Mosaic comes at a fair valuation and a relative discount to its peers, trading under $60 per share. Although the stock’s valuation grade is a C, MOS’s forward P/E of 4.26x is at a 64% discount to its sector peers. MOS has forward EV/Sales of 1.13x, a -26% difference to the sector, indicating that it is relatively undervalued. This stock is priced well at the current price point and its upward trend over several quarters.

MOS Valuation Grade (Seeking Alpha Premium)

On May 18, following news of the U.S. backing the UN’s plan to facilitate grain and fertilizer exports from Russia, Ukraine, and Belarus, fertilizer and grain stocks experienced a slide in prices greater than the broader market. Despite this slide, companies like Mosaic continue to benefit from the conflicts and disrupted exports in Europe, given the need for grain and merchandising. With China recently extending export restrictions, producers like Mosaic should see more significant gains, solidifying its strong buy rating.

The Mosaic Company (MOS) 1-year Trading Chart

MOS 1yr Trading Chart (Seeking Alpha Premium)

MOS Momentum

As you can see from the chart above, MOS has experienced tremendous success over the last year. In reviewing its share price activity and extremely bullish momentum, MOS’s price performance has outperformed the sector median 6x over six months and 22x over nine months, with no slowing in sight.

MOS Momentum Grade (Seeking Alpha Premium)

As we look at Mosaic’s excellent runway and A+ momentum grade, the stock is one of the tops in its sector and industry, consistently outperforming peers on quarterly price performance. As we look to the future of MOS, consider its incredible growth and profitability.

Mosaic Growth & Profitability

Agricultural prices are at multi-year highs with no shortage of need for grains and fertilizers to meet demand. Mosaic focuses on increasing production as the global grain market and exporters face uncertainty amid continued conflicts in Russia and Ukraine. Their collective exports of corn, wheat, and barley have averaged approximately 50 million metric tons per year since 2017.

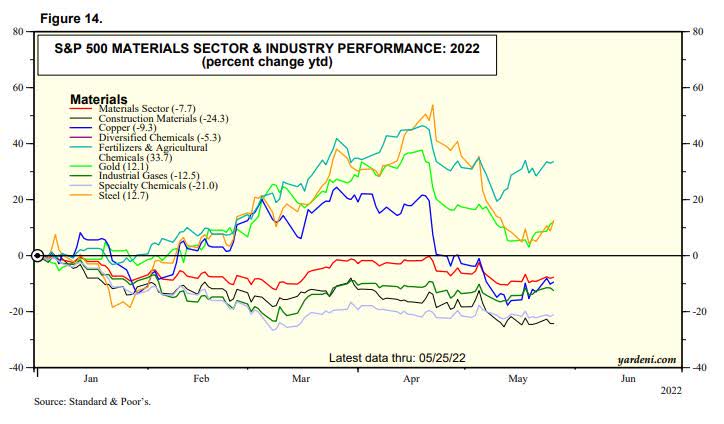

Commodities and fertilizer stocks like MOS have been the benefactors of the conflict abroad and have been significant at inflation-proofing. The chart below shows that fertilizers and agricultural chemicals are up more than 28%.

S&P 500 Materials Sector & Industry Performance: 2022 (Yardeni/S&P)

Mosaic is a top-five potash producer, and as fertilizer prices skyrocket and have taken steps to be more operationally efficient, benefitting from its cost position, ramping up production at its new K3 mine at Esterhazy, and vertically integrating phosphate assets. As the world’s largest phosphate producer, Mosaic mines its own phosphate rock, a crucial feedstock component used to produce such fertilizers. Given year-over-year inflation increases and CPI at 8.3% in April, even if food inflation experiences slowing in the upcoming months, the annual rate for 2022 will be the highest since 2008, translating into some of the sector’s most significant gains.

MOS Growth Grade (Seeking Alpha Premium)

Despite a slight EPS miss in Q1 of $2.41 by $0.01 and revenue of $3.92B, missing by $125M, strong pricing in the sector allowed MOS to offset input costs, and we cannot emphasize enough the increased need for crop nutrients and no slowing in demand. According to SA News, MOS was short of estimates due to logistical constraints that the company said are expected to improve, but linger a little while longer into Q2. Mosaic possesses an A growth grade and A- profitability grade, with year-over-year revenue growth of 52.30%, compared to 26.35% for the sector.

Phosphate segment adjusted EBITDA totaled $632 million, reflecting the impact of strong pricing, which more than offset higher input costs. Potash also benefited from higher prices, as well as the transition to Esterhazy K3, and the elimination of brine inflow management costs. As a result, segment adjusted EBITDA totaled $651 million…Looking forward, we continue to see agricultural market strength extending well beyond 2022,” said Joc O’Rourke, Mosaic President & CEO.

Fertilizers and agricultural chemicals are at the forefront of top stocks and rising prices. Food shortages are sweeping the globe, so there’s time to get in on the action if you missed out on buying this stock when it was trading at an extreme discount. While Mosaic still comes at a fair valuation, as inflation leaves its mark, MOS is a company that will pass costs onto consumers while increasing its profits, making it an attractive stock for portfolios. In my opinion, the pullback from its April high presents a terrific buying opportunity.

3. Chubb Limited (NYSE:CB)

- Market Capitalization: $86.91B

- Quant Rating: Strong Buy

- Quant Sector Ranking (as of 5/24): 19 out of 627

- Quant Industry Ranking (as of 5/24): 2 out of 47

- Dividend Safety Grade: A

A global leader in the insurance industry with more than an $80B market cap, Chubb Limited provides insurance and reinsurance products worldwide. As a result of inflation, better pricing, and industry conditions acting as tailwinds, Chubb experienced great Q1 results, increasing cash flows and an excellent dividend.

Chubb Valuation

Chubb’s written global property and casualty (P&C) premiums increased 11%. Although the company’s D valuation grade is not ideal, we believe the stock is still worth consideration, given its consistent earnings in underwriting profits and global penetration.

CB Factor Grades (Seeking Alpha Premium)

Despite a number of valuation metrics with D grades, the all-important PEG ratio looks good. This ratio combines P/E with growth. Chubb possesses a forward PEG ratio of 0.75x compared to the sector at 1.13, a 33% difference to the sector, earning a Seeking Alpha Quant B+ grade for this all-important multiple. While this stock’s overall valuation grade indicates it is somewhat overvalued, we still see great potential, given attractive growth, profitability, momentum, and revisions grades showcased in the above factor grades.

CB Profitability and Growth

Chubb is on a longer-term upward trend, outperforming the S&P 500 by more than 24% over the last year. As a large insurer, primarily in P&C insurance, this company benefits from substantial growth opportunities and has consecutively beat earnings estimates. Attractive on growth and possessing stellar profitability grades, Chubb is one of the few insurance companies with a global footprint and an influential book of corporate insurance customers, creating a barrier for other insurers, thus decreasing its competition.

CB Earnings (Seeking Alpha Premium)

Q1 2022 earnings resulted in an EPS of $3.82, beating by $0.34. Despite a revenue miss, $9.2B in total net premiums were written, a gain from $8.7B from the prior year. Core operating income beat consensus and P&C underwriting income increased from $622M in Q1 2021 to $1.3B in Q1.

We had an excellent start to the year with record operating earnings and underwriting results, double-digit commercial premium growth accompanied by rate increases in excess of loss cost, and growing momentum in our consumer businesses globally,” -Chubb CEO and Chairman, Evan G. Greenberg.

In addition, $1.2B was returned to shareholders, including $905M in share repurchases and $342M in dividends. The success and incredible momentum have allowed the company to raise its dividend by 4% to $0.83. As we look at the A+ profitability grade, although gross profit margins are not ideal, the company is cash-flush with $11.48B and continued underwriting profits that outperform its peers. As financial journalist Mike Thomas wrote in his article, Chubb Is A Global Leader In An Industry Poised To Outperform The Market:

The company has consistently earned excellent underwriting profits, with its combined ratio topping that of its peers…Chubb has shown strong profitability and an ability to generate large and growing free cash flows, which it has used to increase its dividends for each of the last 28 years.

Chubb has a solid balance sheet, and its forward revenue growth projections of 9% are solid. With additional income streams from commercial and international retail, CB’s commercial P&C premiums increased 15%, with the global retail business seeing a 13% increase in Q4.

Adding insurance to investment portfolios is an excellent diversifier because they are recession-resilient and provide protections that many other sectors do not. Consider adding P&C insurance stocks to your portfolio and energy and commodity stocks for the upcoming Fed hikes.