An almost favorable alternative to consumer staples, the utility sector has performed well in the current environment, serving as a defensive hedge against inflation, particularly, if the odds of a “soft landing” come under pressure.

Along with food and water, people need power, and while astronomical prices and rising inflation will cause consumers to cut back on discretionary spending, they will not stop heating and cooling their homes, nor sit in the dark in the evening. As recessionary concerns, monetary policy, and overall fear continue to create chaos in the markets, the utility sector has been resilient. Compared to the S&P 500 which is down approximately 13% YTD, the Utilities Select Sector SPDR ETF (XLU) is +6% YTD. With geopolitical concerns affecting energy around the world, many utilities have experienced substantial gains and should remain bullish going forward given their defensive nature, which is why we’re focusing our attention on the best utility stocks to invest in for the summer.

Buying Utility Stocks This Summer

Monthly energy costs are spiking primarily due to rising costs, and inflation, in addition to climate concerns. And while volatility in the markets is a test of market psychology on whether to buy the dip or get defensive, utility bills aren’t getting any lower, and homeowners paying $240/month have to budget closer to $400 per month according to Move.org.

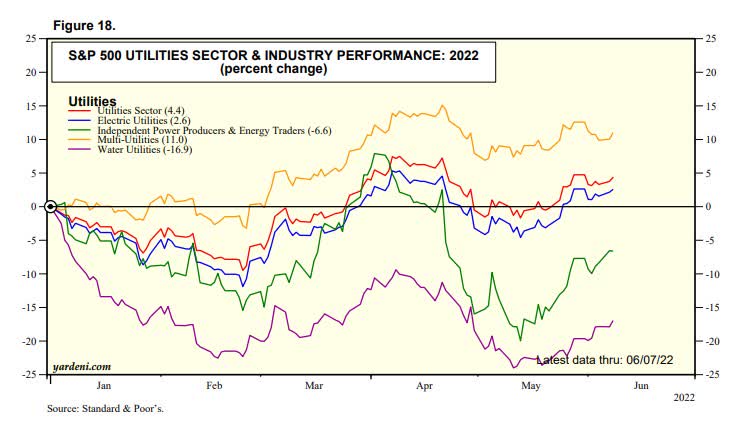

S&P 500 Utilities Sector Performance (Yardeni/Standard&Poor’s)

Utility stocks should provide inflation protection in the form of revenue security. As the cost of energy increases, many utilities can pass costs directly to the consumer, and consumers don’t have much of a choice other than to pay. As you can see in the chart above, the utility sector has gained 4.4% YTD. Consumers are having to pay the price that the market or the utility company sets, hence this is why utilities provide inflation protection.

Utilities also tend to be dividend-paying stocks and in fact, one of the highest dividend-paying stocks from a yield perspective; the dividend for our three stock picks is larger than the average 1.3% dividend of S&P 500 companies, and their dividends are more stable because of the nature of utilities. For this reason, we are highlighting 3 top utilities, which we believe are a strong buy in this environment, to aid in covering your summer air conditioning bill.

1. NRG Energy, Inc. (NYSE:NRG)

- Market Capitalization: $10.97B

- Quant Rating: Strong Buy

- Dividend Safety B+

- Quant Sector Ranking (as of 6/8): 4 out of 104

- Quant Industry Ranking (as of 6/8): 1 out of 41

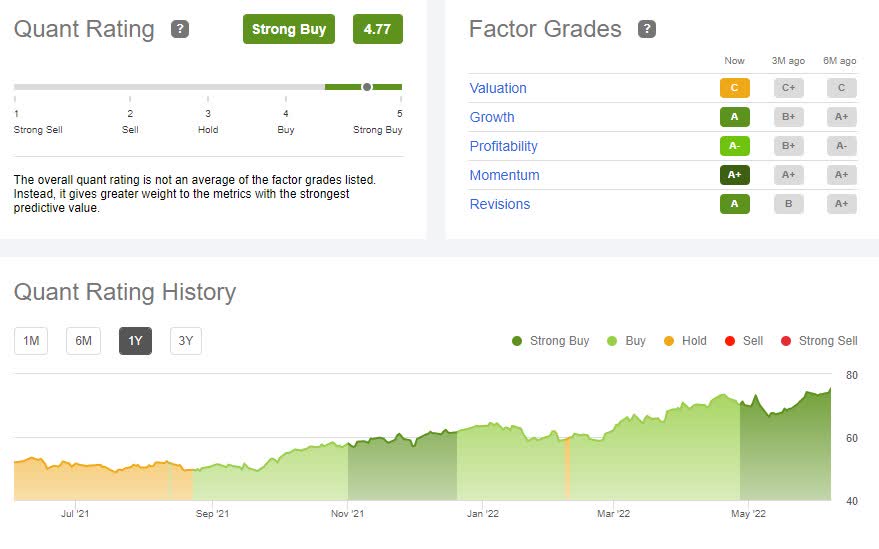

Top value stock, NRG Energy Inc. is an integrated power company that delivers electricity and related products to residents and commercial businesses throughout the U.S., using natural gas, coal, oil, solar, nuclear, and battery storage. In 2021, NRG received the Excellence in Environmental Initiatives SEAL Business Sustainability Awards. Not only is this stock poised for growth and possesses A+ profitability, but its discounted price is also extremely attractive.

NRG Valuation And Momentum

With utilities capitalizing on high inflation and passing costs onto consumers, NRG has had a head start in taking advantage of price hikes, making now a great right time to purchase this strong buy. Bullishly trending and trading nearly 70% below its sector with a P/E ratio of 6.47x, NRG has an overall valuation SA grade of A+.

NRG Valuation Grade (Seeking Alpha Premium)

In addition, the stock has an excellent PEG ratio with a -99.77% difference to the sector and EV/Sales (FWD) of 0.66x. In addition to being undervalued, the stock is +32% over the last year, with continued upward momentum.

NRG Momentum Grade (Seeking Alpha Premium)

With an A Momentum Grade, NRG is outperforming its sector peers quarterly. NRG’s 3-month price performance is more than five times higher than its peers and its six-month price performance is three times higher. If you read my article in January titled NRG Energy: Getting Paid to Wait, there was little clarity on whether the Fed would raise rates. The current outlook makes clear that rates are rising, and waiting to invest may have primed you to take advantage of the growth and profitability this company experiences. Let us dive into the figures.

NRG Growth And Profitability

In addition to a discounted valuation, we consider NRG to have a strong growth outlook with its solid A growth grade. NRG’s growth plan focused on its January 5, 2021, acquisition of Direct Energy in excess of three million additional customers across North America. Additionally, NRG signed 2.6 gigawatts of renewable Power Purchase Agreements (PPAs) that include 45% currently in service in geographically diverse Texas. In addition to the portfolio integration, its revisions grade is solid at a B- and two analyst upward revisions within the last 90 days, following solid Q1 2022 results.

NRG Growth Grade (Seeking Alpha Premium)

Despite an EPS of $0.22 missing by $0.41, guidance remains strong along with revenues of $7.90B. The company has a solid dividend scorecard with nine years of consecutive dividend payments, showcasing that revenue growth is steady. NRG plans to execute on their $1B share buyback program, with increasing energy prices, specifically natural gas serving as tailwinds to deliver increasing cash flows.

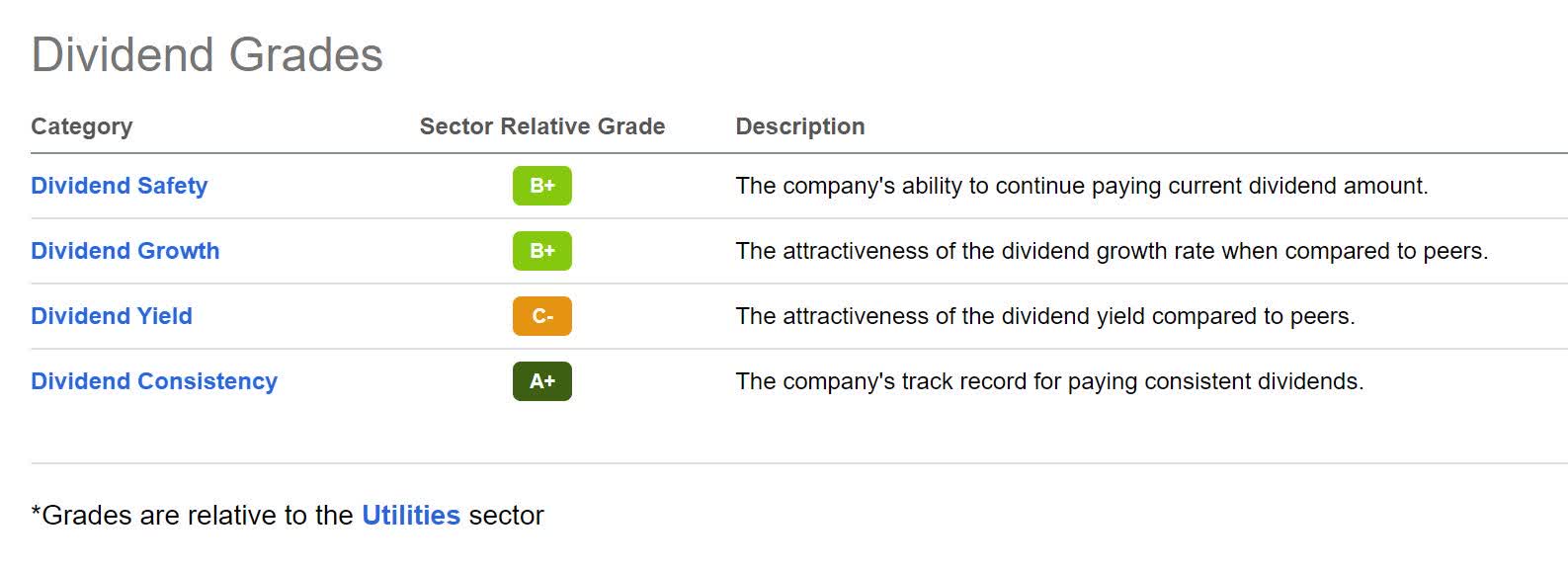

NRG Dividends

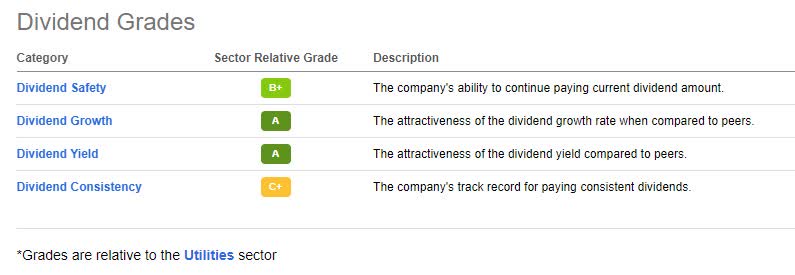

In volatile markets, dividends tend to play an important factor for investors, especially those looking for utilities and steady income. NRG stock has solid dividend grades as showcased below, a 3.03% dividend yield, and a consistent history of paying out a dividend to shareholders which enable investors to offset some of the inflation pains with income generated by these assets.

NRG Dividend Grades (Seeking Alpha Premium)

There are a number of attractive utility stocks to choose from. As fellow Seeking Alpha Contributor, The Black Sheep writes, “Electricity prices are at their highest level in a decade, and the pricing power NRG has proven over the past year is another reason to be bullish on the stock,” and our next two picks.

2. Vistra Corp. (NYSE:VST)

- Market Capitalization: $11.44B

- Quant Rating: Strong Buy

- Dividend Safety: B-

- Quant Sector Ranking (as of 6/8): 1 out of 104

- Quant Industry Ranking (as of 6/8): 1 out of 8

A top momentum stock, Vistra Corporation (VST) has A+ momentum that is crushing its sector peers on quarterly price performance, and solid overall factor grades to match, as showcased below. Factor grades instantly compare a stock’s investment characteristics to its sector, and it’s clear with the A+ through B- ratings, that VST is on top of its class!

VST Factor Grades (Seeking Alpha Premium)

Together with its subsidiaries and serving more than 4.3 customers nationwide, Vistra is in the business of retail electricity and natural gas, wholesale energy purchase and sales, and commodity risk management. With tremendous momentum, VST is not only outperforming the S&P 500 by nearly 50%, but its peers are also way behind.

Vistra Valuation And Momentum

Vistra is strongly bullish with many analysts stating the stock is overbought given the number of active purchases driving the stock price higher. When you look at the below column for percentage difference to the sector, each quarter, VST is crushing the competition, with an astounding nine-month price performance of 1,111.07% better than its sector.

VST Momentum Grade (Seeking Alpha Premium)

If that’s not enough to convince you that this stock is on a roll, YTD the stock is +17%, and over one year +47%. In addition to bullish momentum, VST comes at a discount with forward P/E of 11.92x, a -41.82 difference to the sector, and current EV/Sales and EV/EBITDA are discounted by more than 40%, an indication this stock is extremely undervalued. With all of these variables to consider, when for sources of income to offset some of the spiking energy costs, dividends can add an extra layer of appeal.

VST Dividends

Vista has been steadily growing over the years and reduced a substantial amount of debt in 2019-2020 allowing them the financial flexibility to repurchase stock and raise their dividend. Vista’s overall dividend grades are solid and its executive team is committed to maintaining a strong balance sheet with substantial liquidity for cash on hand to execute on the $2B share repurchase program and continued commitment to shareholders.

VST Dividend Grades (Seeking Alpha Premium)

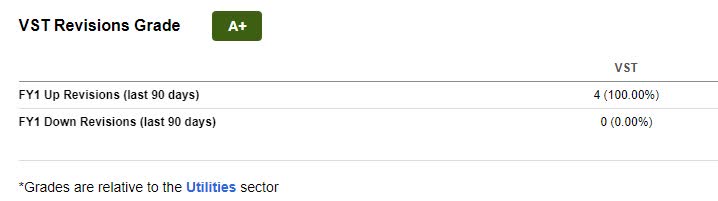

Although recent earnings were a miss, 4 analysts gave the company FY1 Up revisions, and Vista declared a $0.177 quarterly dividend, which was an increase of 4.1% from the previous.

VST Revisions (Seeking Alpha Premium)

VST Growth And Profitability

Despite the Q1 2022 earnings miss, the results were in-line with expectations and the company’s outlook remains strong, focused on strategic priorities that involve the desire to expand as a bigger supplier globally, with the world energy constraints serving as tailwinds. In addition, ESG and strong demand and geopolitical factors should allow VST to take advantage of higher natural gas and power prices.

Frankly, in my 40 years, I have not seen a confluence of events quite like this. Certainly, Vistra is in the right position to capitalize on the strong forward curves. The effectiveness of our execution will be key as the day-to-day volatility is extraordinary. It is a rare opportunity presented to us and it is our job to create the most value out of it while managing the risk.” – Curt Morgan, CEO of Vistra

We are starting the year with a focus on execution. We delivered Adjusted EBITDA in the quarter in line with company expectations with increasing confidence in full-year 2022, are executing on a comprehensive hedging strategy to capitalize on the beneficial power and commodities markets that is expected to provide significant value to Vistra in 2023 and beyond, and are continuing the advancement of our capital allocation priorities, returning capital through stock repurchases and paying a meaningful and growing dividend.” – Curt Morgan, CEO of Vistra.

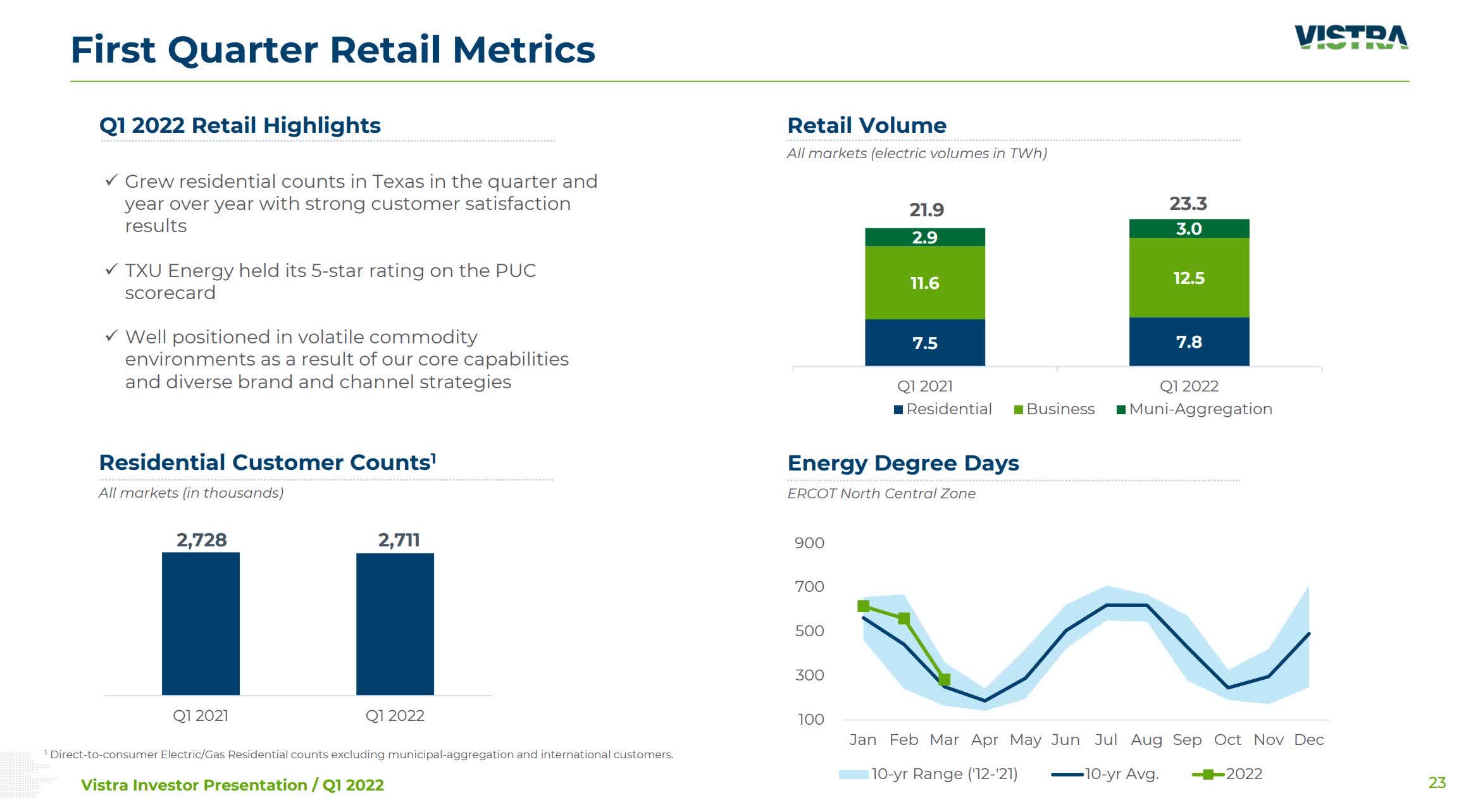

Vista has several development projects in the works, and Q1 retail metrics have been strong, allowing the company to maintain its 5-star rating and navigate the volatile commodity market.

Vistra Q1 Retail Metrics (Vistra Q1 2022 Investor Presentation)

As the energy and commodity landscape bodes well for this stock, the bull case is pretty straightforward and supports Vistra management’s guidance of $2.8-3.3B in 2022 EBITDA with “free cash flow before growth” between $2.1B and $2.6B this year. Sitting on more than $2B cash from operations and the company hedging some of their energy price exposure and setting prices, VST should continue to generate stable cash flows while continuing on an upward trend while coming at a severely discounted price.

3. National Fuel Gas Company (NYSE:NFG)

- Market Capitalization: $6.78B

- Quant Rating: Strong Buy

- Dividend Safety: B+

- Quant Sector Ranking (as of 6/8): 2 out of 104

- Quant Industry Ranking (as of 6/8): 1 out of 13

Natural Fuel Gas is a diversified, vertically integrated natural gas utility company. With its exploration and production generating nearly 50% of its EBITDA, midstream generating 36% EBITDA, and its utility segment 15%, NFG rallied to new highs following Russia’s invasion of Ukraine. Continuing to benefit from strong demand, NFG has benefited from a rally in the average realized price of natural gas of approximately 18%.

“As a result, it grew its earnings per share by 40% over the prior year’s quarter, from $1.06 to $1.48, and exceeded the analysts’ estimates by $0.15. Notably, the company has exceeded the analysts’ estimates for 11 consecutive quarters. This is a testament to the sustained business momentum of the company and its strong business execution,” writes Seeking Alpha Author Aristofanis Papadatos.

Not only does this stock have great characteristics, but when you look at the underlying metrics that comprise the below quant ratings and factor grades, they are quite impressive, hence, NFG’s strong buy recommendation.

NFG Quant Ratings and Factor Grades (Seeking Alpha Premium)

NFG Valuation And Momentum

Despite a C valuation grade, NFG is bullishly trending with A+ momentum. Year-to-date the stock is up 17% and over the last year +38%. NFG has a forward P/E of 12.46x, a -40.96% difference from its sector peers, and an A+ PEG (TTM), indicating that it is relatively undervalued. At the current price point and its upward trend over the last several quarters, this stock which continues to price in improved earnings for 2022, is in a great position.

NFG Valuation Grade (Seeking Alpha Premium)

NFG Growth And Profitability

Like many energy and utility companies, NRG has experienced stellar growth and profitability post-pandemic following skyrocketing prices, geopolitical issues abroad, and consistent demand. Operating results were up 25% year-over-year, and recent EPS of $1.68 beat by $0.06 and revenue of $701.72M beat by $49.44M, an increase of 27.33% YoY.

NFG Growth Grade (Seeking Alpha Premium)

NFG has been very strategic in its operations to ensure operational and financial success. With the difficult regulatory environment in California, NFG recently opted to sell its Sentinel Peak located in California for $280M in cash and $30M contingent consideration.

NFG Profitability Grade (Seeking Alpha Premium)

The sale of this asset should result in approximately $175M to $200M after taxes. With the profits of the sale added to its balance sheet, the company’s overall profitability grade stands to be further bolstered. As you look at the A- grade above and underlying metrics, the sale should make shareholders even happier, adding to its amazing track record of consistently paying its dividend.

NFG Dividends

National Fuel Gas is one of a few dividend kings, having paid a dividend for 119 consecutive years and has raised its dividend for over 50 consecutive years. Offering a forward dividend yield of 2.41%, this stock’s dividend growth streak is beyond impressive.

NFG Dividend Scorecard (Seeking Alpha Premium)

NFG has a strong balance sheet, healthy payout ratio, and a B+ dividend safety rating. Income-oriented investors looking for a steady stream of consistent payouts to help offset inflationary concerns, look no further! NFG along with our other two picks are strong buys and have excellent fundamentals.

Conclusion

Capitalizing on companies like integrated utilities, natural gas, and renewables is a great opportunity for the future. As the renewable energy and utility market share grow, it increases the value of our stocks’ generation assets. Utility companies may not be considered a sexy industry, but stocks like NRG, VST, and NFG are necessary and provide value to investors seeking low volatility, income-producing, defensive stocks for their portfolios in the current environment, where fear is moving the markets.

Looking forward, as investors look to companies that can weather increasing inflation and for stocks that should be able to cover their dividends, consider using our Quant screeners to help you find superior stocks in every corner of the markets, including our selection of Top Dividend Stocks.