Suppose you’re looking at dividends as a determinant for quality. In that case, you have to look not just at the yield but beyond the level of yield and dive into consistent contributors to performance such as track record, dividend safety, and dividend growth.

There’s a correlation between strong dividend growth and strong equity returns. Solid dividend growth and reinvested dividends are indicators of strong equity returns. Although yields ranging from 5.15% to more than 20% are high, many companies have these types of yields, and we are focusing on four stocks that also have solid growth, and strong capital gain potential:

- Golden Ocean Group Limited (NASDAQ:GOGL) – 12.45% Div Yield (FWD)

- Star Bulk Carriers Corp. (NASDAQ:SBLK) -20.58% Div Yield (FWD)

- W. P. Carey Inc. (NYSE:WPC) – 5.15% Div Yield (FWD)

- STORE Capital Corporation (NYSE:STOR) – 5.60% Div Yield (FWD)

High Yield Monsters with Low Risk

High yield monsters, or as most investors deem them, high-yield dividend stocks yield above 5% with a quant rating of Buy or Strong Buy and are considered reliable investments. Investors want quality dividend stocks that are fundamentally strong with solid earnings projections. As fear moves the markets, uncertainty surrounding monetary policy, inflation, and rising fuel and energy prices is paving the way. Passive income helps ease some investors’ concerns. The right combination of value, growth, and yield can make for an excellent investment despite down investor sentiment.

By focusing on stocks with higher dividend yields than the S&P 500, whose forward dividend yield is at 1.33%, you’ll find that companies that possess high yields can provide regular passive income to offset the historically high inflation we’re experiencing. Let us dive into our first stock pick.

4 Dividend Stocks with High Yields to Invest In

Not all dividend stocks are created equal. Given that yield is a payout relative to share price, which does not always mean the company is doing well when picking high-yield stocks, investors must dig deeper into a stock’s fundamentals. Consider these five stocks that showcase solid financials and overall fundamentals that complement their high yields to stand the test of time.

Investing In Shipping Company Stock

The first two stocks are in the shipping sector, as there’s a ton of pent-up demand given recent lockdowns in China and some of the largest global ports. Given the supply chain disruptions and backlog, coupled with inflation, consumers are absorbing the price increases, and we have the dividend stocks to try and offset some of these prices with a steady flow of income. Check out our first two strong buys.

1. Golden Ocean Group (GOGL)

- Market Capitalization: $3.15B

- Quant Rating: Strong Buy

- Dividend Safety Grade: C

- Forward Dividend Yield: 12.45%

Owner and operator of 81 dry bulk vessels, Bermuda-based shipping company Golden Ocean Group Limited (GOGL) operates and transports vessels that contain bulk commodities like ores, coal, grains, and fertilizers. With inter shipping demand in high gear, the stock is on an upward trend, +57% YTD and over the last year, +50%.

“The company expects freight rates to increase in the upcoming quarters as it expects dry bulk fleet demand to outpace dry bulk fleet supply. Comparing Golden Ocean’s leverage ratios with some peers indicates that the company has a healthy leverage condition,” writes Seeking Alpha author SM Investor.

GOGL Momentum Grade (Seeking Alpha Premium)

In reviewing Golden Ocean’s stellar momentum grades, its price-performance outperforms its sector peers by more than three, four, and five times! In addition to excellent momentum, GOGL comes at an extreme discount.

GOGL Valuation

Golden Ocean Group possesses an incredible valuation framework. With an A valuation grade, GOGL’s forward P/E ratio of 5.89x is 66% below its sector peers. Its current PEG ratio of 0.01x is a -98.53% difference to the sector. The stock showcases an excellent EV/EBITDA (TTM) of 6.29x, nearly 50% below its peers, indicating it is severely undervalued.

GOGL Valuation Grade (Seeking Alpha Premium)

The stock comes at an excellent price with tremendous momentum. Still, Golden Ocean Group’s growth and profitability are also strong indicators that the attractiveness of the company’s dividend yield, growth, and ability to continue paying a dividend should stand the test of time. Let’s dive into the numbers.

GOGL Growth And Profitability

Golden Ocean is experiencing tremendous growth, with tailwinds from increasing costs that include freight rates and industrials benefit from demand upswings. Because industrials are a diversified sector, reducing its concentration risk, as I wrote in The Hunt for Quality: Best Profitable Stocks to Invest In, “domestic production in March saw a 0.9% increase and outpaced market forecasts. April of this year crushed figures when it posted its highest monthly volume in 100 years of 105.59, according to the Federal Reserve’s Industrial Production Index: Total Index.”

GOGL EPS (Seeking Alpha Premium)

For five consecutive quarters, GOGL has beaten both top-and bottom-line earnings, with the most recent resulting in two analyst upward revisions in 90 days. EPS of $0.53 beat by $0.16, and revenue of $208.91M beat by $21.20M, an increase of 75.82% year-over-year. This company possesses a strong growth outlook, but profits have also continued to be strong, with GOGL sitting on $677.44M in cash from operations.

GOGL Profitability (Seeking Alpha Premium)

“In Q1, we recorded an EBITDA of $149 million, which resulted in a net profit of $125 million, or $0.63 per share. We achieved average time charter equivalent rates of $24,800 per day for the Capes and 23,600 for the Panamaxes…Looking at this quarter, Q2, we have so far secured $28,000 per day for 78% of our Cape days, $27,000 per day for 77% of our Panamax days. Looking ahead and into Q3, we have secured $38,000 per day for 15% of our Cape days and $35,000 per day for 33% of our Panamax days.” –Ulrik Anderson, GOGL CEO.

With its robust balance sheet and discounted valuation, GOGL is sitting pretty. They refinanced their debt and lowered their cash breakeven. They also pay a substantial portion of their net profits in dividends. This stock, along with our next pick, is a strong buy.

2. Star Bulk Carriers Corp. (SBLK)

- Market Capitalization: $3.34B

- Quant Rating: Strong Buy

- Dividend Safety Grade: B-

- Forward Dividend Yield: 20.58%

With its most robust Q1 Earnings results ever, prompting a $1.65 dividend payout, global cargo shipping company Star Bulk Carriers Corp. (SBLK) is one of my favorite Shipping Stocks to Buy Amid the Global Shipping Crisis. With continued tailwinds, tremendous momentum, and a 20.58% forward dividend yield, SBLK continues to be on an upward trend, surely making shareholders happy.

A global cargo shipping company of bulk materials like iron ore, coal, grains, fertilizers, and steel products, this stock has capitalized on the shipping crisis involving some of the largest hubs in the world like Shanghai and the maritime and port authority of Singapore. ProShares CEO Michael Sapir says it best,

“The pandemic didn’t just highlight the crisis facing the global supply chain, it identified a ripe opportunity to invest in the companies striving to provide real solutions and embrace new technologies that may revolutionize global trade.”

This shipping stock is rated a strong buy, as evidenced by its fundamentals, quant ratings, and factor grades. Look at SBLK’s Factor Grades and quant ratings below, which characterize the stock’s value, growth, profitability, momentum, and EPS revisions relative to its sector peers.

SBLK Quant Ratings (Seeking Alpha Premium)

SBLK Valuation & Momentum

This stock has an A+ overall valuation grade and comes at an extreme discount, trading below $32/share, with a forward P/E ratio of 4.82x, a -72% difference to the sector. SBLK’s current PEG is at a -99.40% discount to the sector.

SBLK Momentum Grade (Seeking Alpha Premium)

When comparing the company’s six-month, nine-month, and one-year price performance, SBLK is two, three, and even five times better performing than its peers, indicating this stock’s bullish momentum. In addition to these metrics experiencing upward momentum, SBLK’s growth and profitability are also favorable.

SBLK Growth And Profitability

SBLK’s recent earnings were astounding, given it had a previous Q4 EPS of $2.96 beat by $0.44, and revenue of $427.64M beat by nearly 200%. Like many dry bulk shipping companies post-pandemic, SBLK has been crushing earnings, has been on an upward trend, and is trading near its 52-week high of $33.99/share. The stock is +34% YTD, and its one-year price performance is +54%.

SBLK Growth Grade (Seeking Alpha Premium)

The latest Q1 2022 earnings were just as impressive, with an EPS of $1.72 beating by $0.32 and revenue of $307.48M beating by $31.28M, 91.68% year-over-year.

“Our last 12 months adjusted EBITDA is at $1.04 billion and adjusted net income of $831 million. At the same time, we have returned a cumulative dividend of $576 million to our shareholders…Our time charter equivalent rate was $27,405 per vessel per day. Our combined daily operating expenses and net cash G&A expenses per vessel per day amounted to $5,812. Therefore, our TCE, less OpEx and G&A, is around $21,600 per day per vessel…Star Bulk has been able to significantly outperform the adjusted peer average by more than $5,000 per day per vessel, implying an annual EBITDA overperformance of more than $230 million on a 128 vessels fleet and demonstrating how assets are efficiently utilized in the Star Bulk platform.” –Simos Spyrou, Star Bulk Co-CFO.

With the increasing demand for shipping and the backlog of industrials and goods in ports, the two shipping stocks mentioned should maintain their bullish trends and remain profitable through 2022. Not only are these stocks rated strong buys according to our quant ratings, but let us dive into a few high-yielding REITs.

Investing In Real Estate Stocks for Steady Income

As the third-largest asset class in the U.S. and one of last year’s top-performing sectors, REITs offer dividend benefits and portfolio diversification. Our three final picks have bustling cash for operations and come at relative discounts, with promising growth and profitability outlooks.

3. W. P. Carey Inc. (WPC)

- Market Capitalization: $16.01B

- Quant Rating: Buy

- Dividend Safety Grade: C+

- Forward Dividend Yield: 5.15%

I wrote about W. P. Carey Inc. (WPC) in an article titled 3 Best REITs to Buy to Fight Inflation, given that 2022 paved the way for real estate stocks as top choices for investment amid heightened market volatility. Offering higher yields, better values, and strong growth and profitability outlooks, REITs tend to do well in a rising rate environment, especially as compared to bonds.

“Rising rates generally means the economy is growing, which translates into greater demand for real estate and the ability to charge higher rent. Interestingly, a 40-year analysis by Nareit found that REITs performed well during both high inflation and low inflation periods. This means they are less subject to prediction risk, or the risk that investors correctly predict high-inflation periods.” –Jenna Ross of Visual Capitalist.

W. P. Carey Inc. is on an upward trend and ranks among the largest net lease REITs with more than $16B in market capitalization and a diversified commercial real estate portfolio. Focused on premier single-tenant warehouses, office, retail, and self-storage units, WPC’s bullish momentum results from the tailwinds provided by rising inflation and recessionary fears. Investors want investments that can provide income, and with an A+ dividend consistency grade and 24 years of consecutive dividend payments, this stock is ripe for the picking.

WPC Valuation & Momentum

WPC comes with a solid valuation grade of B and is trading in line with sector peers. Fellow Seeking Alpha Marketplace author Brad Thomas writes, “We believe that the market is underappreciating WPC’s growth prospects and, therefore, the stock appears to be irrationally cheap.”

WPC Momentum Grade (Seeking Alpha Premium)

The company’s share price has seen a moderate increase of +3% YTD and nearly 8% over the last year. Looking at the above Momentum, WPC is outperforming its sector peers substantially every quarter.

WPC Growth & Profitability

Higher inflation should benefit WPC’s growth, allowing it to trickle down price increases onto its customers. As the Fed raises rates, rental rates can be shifted onto tenants so that the price of maintenance services and taxes do not affect WPC’s bottom line.

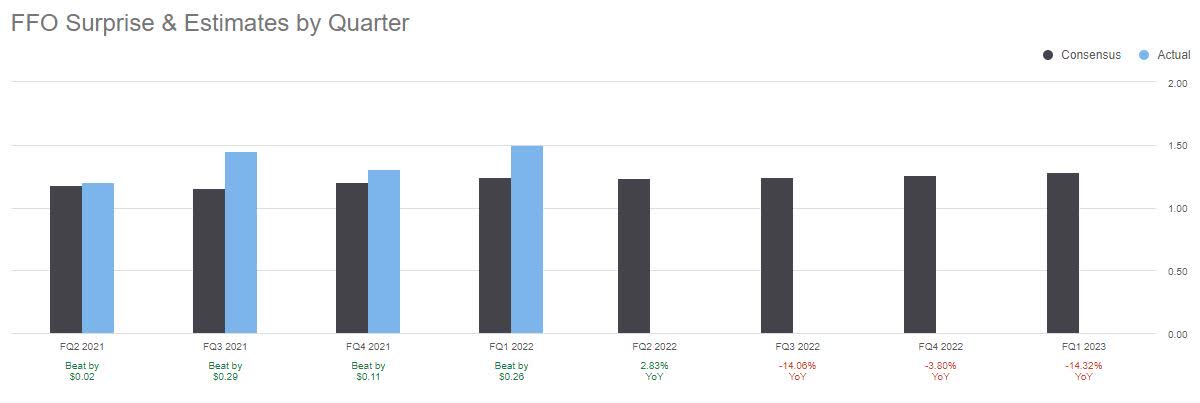

WPC FFO Surprise (Seeking Alpha Premium)

WPC’s diverse tenant holdings and geographic locations have allowed it to continue posting double-digit growth. The most recent Q1 2022 results reported sales of $348.44M, a year-over-year increase of nearly 12%, and AFFO of $1.35/share, a rise of 10.7%.

“The strong year-over-year AFFO growth we reported this morning reflects both our sustained higher investment activity and inflation beginning to more meaningfully flow through to our rents…our cost of equity has improved meaningfully since late February with our stock currently trading around its highest level since late 2019, before the onset of COVID.” -Jason Fox, WPC CEO.

I normally do not write about companies that are in the process of a merger. Given WPC’s strong outlook and as one of the largest REITs in the MSCI US REIT Index, its CPA:18 merger appears to be a factor that will strengthen the bull thesis. This merger is the third installment of CPA’s managed funds. A non-traded REIT that seeks to generate income while preserving investors’ wealth through diversified holdings, CPA:18 has been under the advisement of WPC for nearly a decade. CPA:18 is the final traunch of managed funds that WPC has been winding down since 2014. WPC acquired CPA:16 for $4B in 2014; CPA:17 for $5.9B in 2018, and now it’s planning its purchase of CPA:18 in a cash-and-stock deal for $2.7 billion, making it well-positioned to continue capitalizing in the current and future environment. Positioned to continue fighting inflation and post higher year-over-year FFO, we believe WPC will maintain its buy rating well into the future, along with our next REIT.

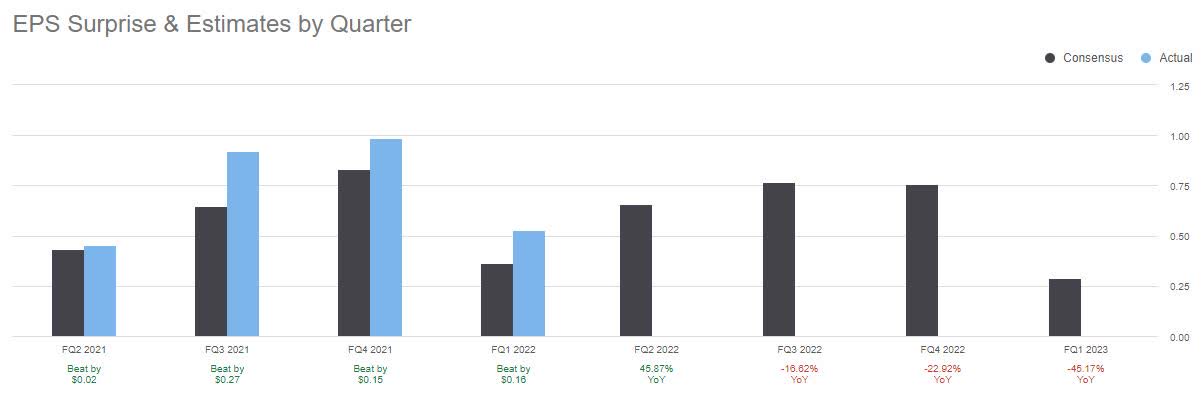

4. STORE Capital Corporation (STOR)

- Market Capitalization: $7.63B

- Quant Rating: Strong Buy

- Dividend Safety Grade: B

- Forward Dividend Yield: 5.60%

One of the largest and fastest triple net lease REITs with an enterprise value of $12.2B and more than 2,500 properties, STORE Capital Corporation (STOR) is diversified and focused on Single Tenant Operation Real Estate. On a longer-term bullish trend, with bullish momentum, STOR’s trading volume continues to increase, prompting analysts to consider the stock overbought, making clear that investors want this investment and are actively purchasing shares, driving the price higher.

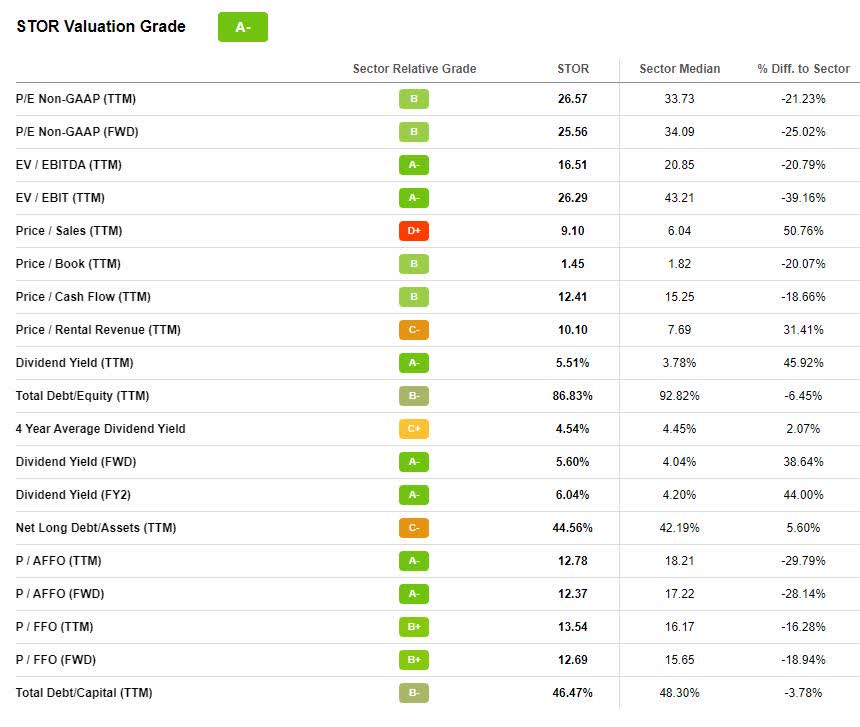

STOR Valuation Grade (Seeking Alpha Premium)

With an A- Valuation Grade, the stock is undervalued compared to sector peers. The stock is trading at a current EV/EBITDA of 16.51x, a -20.79% difference from the sector, and possesses a 13.54x Price to FFO while offering investors a forward dividend yield of 5.60%. This stock makes a compelling argument for being a strong buy. In addition to a strong dividend yield, its overall dividend grades are attractive, which is the focus of this piece. Investors want high-yielding monsters with solid dividends.

STOR Dividend Grades (Seeking Alpha Premium)

As we look at the dividend safety of STOR, not only does the stock get a B rating for its ability to continue paying a current dividend, the company has had a consistent dividend growth rate for nearly a decade. As a result of recent earnings growth and substantial profits, analysts have boosted STOR’s 2022 guidance.

STORE Capital Growth & Profitability

With high inflation and the Fed plans to raise rates to counter inflation, concerns are mounting that recession may be around the corner. STOR’s triple net lease REITs tend to be more conservative, possessing strong balance sheets and diversification to weather drawdowns. STORE Capital’s outlook is optimistic as evidenced by the below revisions grades, prompted by the latest stellar earnings results.

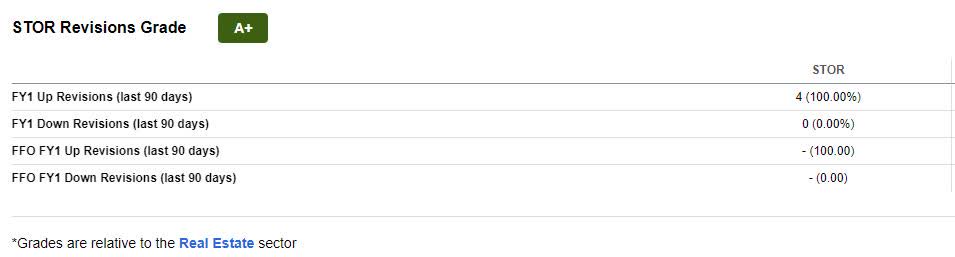

STOR Revisions Grade (Seeking Alpha Premium)

After posting Q1 FFO of $0.57 and revenue of $222.12M, a year-over-year increase of 21.9%, the company raised its 2022 AFFO per share guidance from $2.18 to $2.22 to a range of $2.20 to $2.23 and raised its 2022 annual real estate acquisition volume guidance, net of projected property sales, from a range of $1.1 billion to $1.3 billion, to a range of $1.3 billion to $1.5 billion.

“While rising interest rates can reduce incremental profitability by squeezing investment spreads and also lead to multiple compression on the stock price, cap rates generally follow interest rates higher over time. As a result, triple net lease REITs typically have the profit margins on incremental property acquisitions restored within a few quarters. REITs are then able to lock in these higher cap rates over multi-decade contracts while they can relatively easily refinance the debt attached to them whenever interest rates decline again. The net result is improved profitability.” –Samuel Smith, Seeking Alpha Marketplace Author.

With the current inflationary environment and discounted price, STORE Capital’s excellent financials have resulted in raised guidance. Our other three picks should also be considered for portfolios if you’re seeking top-yielding stocks with solid dividends.

Conclusion

Investors want the best stocks when markets rise or fall, and when buying high-yield stocks, they should be able to thrive in both environments. Be on alert for dividend stocks with high yields that will not sacrifice quality or growth.

Each of our stocks is a win-win for value and growth investors, possesses solid forward growth outlooks, is undervalued, and should provide investors with a steady income stream in this highly volatile market. In addition to solid dividend safety grades, each of our four recommendations, GOGL, SBLK, STOR, and WPC, has great dividend yields and excellent cash for operations, ensuring these stocks remain upward.

Our investment research tools help to ensure you’re furnished with the best resources to make informed investment decisions. Check out the Dividend Grades on your favorite stocks and evaluate them using our tools that can help you make tactical investment decisions that ensure you stick with dividend income that is strong and stands to increase over time. In this volatile environment, consider using Seeking Alpha’s ‘Ratings Screener’ tool to help you achieve diversification into desired sectors you like, including energy or commodities.