Since the outbreak of COVID-19, the NBS has been conducting impact surveys, assessing the welfare of Nigerians. The latest survey conducted in Jan-2021 provides insight into how the Nigerian economy has gradually recovered from the effects of the Covid-19. A sample of 1,346 households were assessed for this report.

Firstly, the report highlighted how unevenly Covid-19 hit children’s education. Around 48.0% of children surveyed in the lowest quintile had no access to educational content in the 15 days preceding the interview compared to just 14% in the richest quintile. Regarding galloping food prices, a pertinent issue, the survey is consistent with the recent consumer price index and inflation data.

Households, when asked if the prices of the major food items they consumed had increased compared with one year ago (Jan-2020 vs Jan-2021), 79.0% of households that needed to buy rice indicated that the price of rice increased.

On working status, the overall share of respondents who gainfully employed was at 70.0% in Jan-2021. A massive improvement from the low point of just 43.0% in April 2020.

Although the survey provides some bleak updates, it ends with a silver lining, which may indicate that with the return of economic activities, the effects of Covid-19 on the workforce is beginning to abate. The report showed that in Jan-2021, around 38% of households surveyed had experienced income losses, perhaps a sign of a rebound compared to 70.0% in the early days of the pandemic.

For our take, while we believe that the reopening of the economy would lead to a slight recovery in activities, we struggle to see headroom for sustained accelerated growth unless various stakeholders within the economy come together to solve the inequality and structural problems exposed by Covid-19.

Fidelity Bank Plc has announced its financial results for the year ended December 31, 2020. The performance which capped a remarkable year showed strong growth in Core Operating Profits, Net Revenue, and other key financial indices.

Financial Review

Gross Earnings declined by -5.4% to N206bn from N218bn in the previous quarter.

Profit before tax declined by 7.6% to N28bn from N30.4BN in 2019FY due to an increase in the Bank’s loan provisions to shield it from any headwinds. A positive for the Bank especially in the current era of Covid-19 and its attendant effect on business risks.

Profit after tax declined by 6.2% to N26.650bn from N28.425bn

Customer Deposit rose by 38.7% from N1,225.2BN to N1,699.0BN

Total Assets grew by 30.5% from N2,114.037TRN in 2019 FY to N2,758.148TRN.

Net Assets grew by 16.9% from N234bn to N274bn.

In respect of the 2020 financial year, the Board of Directors recommends a dividend of 22 kobo per Ordinary Share of 50 kobo each amounting to N6,371,768,852 for approval at the Annual General Meeting.

If approved, the dividend will be paid to Shareholders whose names appear on the Register of Members at the close of business on April 16, 2021. The proposed dividend is subject to Withholding Tax at the applicable tax rate, which will be deducted before payment.

“We are pleased with our financial performance, which clearly showed the resilience of our business model as core operating profit increased by 50.9% to N44.9BN from N29.8BN in 2019FY.

We also saw a significant improvement in our efficiency indices as the cost-to-income ratio moderated downward to 65.1% from 73.4% in 2019FY. However, Profit Before Tax (PBT) dropped by 7.6% to N28.1BN as we proactively increased our provisions on risk assets to N16.9BN from a net write-back of N0.6BN in 2019FY,”

The CEO added that the bank

“Took a conservative stance in recognition of the impact of the global pandemic, which has redefined business risks and opportunities in the new normal”.

As seen in recent years, the Bank’s digital retail banking approach has continued to yield positive results. Though Digital Banking income dropped by 18.8% due to the revised banker’s tariff, it increased by 19.6% QoQ on account of increased customer adoption as more services were migrated to the Bank’s digital channels.

Onyeali-Ikpe is happy with the progress of its digital banking play stating that over 52.8% of customers are now enrolled on the Bank’s mobile/internet banking compared to 47.4% in 2019FY, while 88.4% of our customers’ transactions were done on the digital platform products and more than 81% of total transactions done on digital platforms.

Mr. Adekunle Sonola joined Union Bank in 2015 as an Executive Director in charge of the Bank’s Commercial Banking business.

Mr. Adekunle Sonola | www.wordpress-1516176-5827464.cloudwaysapps.com

He has more than 26 years of experience in the banking sector. Prior to joining Union Bank, he worked at Guaranty Trust Bank where he rose from being a member of the Corporate Finance Group to Divisional Head, Corporate Banking.

He left Guaranty Trust Bank as Managing Director, East Africa, where he successfully rolled out the franchise in Uganda, Rwanda and Kenya. He has also served as Director, Investment Banking Africa for Standard Bank of South Africa.

Mr. Sonola holds a Bachelor’s Degree in English from Ogun State University, Nigeria, an LL.B in Law from Obafemi Awolowo University, Nigeria and an MBA from Durham University Business School, Durham, United Kingdom.

The Board of Union Bank is thankful to Mr. Sonola for his years of service and his many accomplishments while at the Bank.

Established in 1917 and listed on the Nigerian Stock Exchange in 1971, Union Bank is a household name and one of Nigeria’s long-standing and most respected financial institutions.

The Bank has a network of over 300 Sales and Service Centres across Nigeria.

Following recapitalisation in 2012 from new investors and a new Executive Management team, Union Bank has undergone an award-winning transformation programme to re-establish the bank as a leading provider of financial services in Nigeria.

Union Bank is focused on Retail, Commercial and Corporate Banking businesses. In addition to standard current and savings product portfolio, Union Bank has launched pioneering products into the Nigerian retail market including Union Korrect, Union Goal and Union Betta.

If You Are Not Making Money, You Should Not Lose Money – Bisi ONI

As Nigeria is facing economic instability and as the inflation rate is growing astronomically, experts in the financial sector put thoughts together and provided some solutions to the economic recession Nigeria is wallowing in for the past few years.

In a webinar Organized by FundQuest Financial Services Limited on 27th of March titled: The Road to Recovery, The Nigerian Economy and You, the Keynote speaker, Mr. Ugo Obi-Chukwu popularly known as “Ugodre”, founder Nairametrics; Mr Bisi Oni, Executive Director/COO, FundQuest Financial Services Limited and Mr. Abiodun Akinjayeju, Managing Director, FundQuest Financial Services Limited all called for the need to sustainable policies to drive the economy.

In the last few years, Nigeria has seen rising inflation, recessions and of course, the unemployment rate in the country continues to grow since 2018 and as of December 2020, a total of 12.72 million Nigerian youths were out of jobs.

Speaking on the challenges of the country, the Chief Speaker, Ugo Obi-Chukwu said Nigeria is indeed facing a lot of issues ranging from Stagflation, high unemployment, high poverty, insecurity, social unrest and zero trusts in government.

According to him, Nigeria has been in Stagflation, high inflation or galloping inflation with a tepid GDP growth rate for the past 5 years which he admitted is one of the worst economy malaises a country can have. “The UK faced it in the late 70s, most European countries can’t imagine stagflation in their country, but we have been in stagflation in the past 5 years,”he said.

He said the unemployment rate that is on the rise in Nigeria is the consequence of stagflation and when it’s happening, it’s not a surprise which is a sign of abject poverty.

While analyzing how the economy is plunging, Mr. Ugo mentioned that towards September 2019 when the government announced the border closure, food prices started going up gradually and in March 2019, as a result of the COVID-19 and drop in oil prices things starts to get worse and towards October, Nigeria experienced rumour of increase in electricity prices and in June and August, there was a major devaluation, and all these filtered into the cost of goods and services.

He continued that as the effect of herdsmen crises continues to rise, it affected the cost of food prices and food inflation keeps rising. The inflation rate which is at 17.33% he said may likely reach 20% this year as a result of the fuel subsidy been debated, electricity tariff which could go up and a likely devaluation this year depending on where oil price sits.

The Unemployment rate according to him has gotten worse since 2018 and in 2021 reached 33.3% where about 10 million people dropped out of the workforce and as of December 2020 total of 12.72 million Nigerians youths are out of jobs. ‘We have high unemployment because of the high inflation rate and our GDP is poor”he said.

Other challenges include increase insecurity ranging from terrorism, banditry which has affected the free movement and transportation of goods; social unrest like the EndSARS movement which was driven by the youth; ill-timed fiscal policies, bad governance, poor infrastructure amongst others.

He frowned at how Nigerians depend mainly on importation without making significant exports to earn forex. “Everything we like to consume here, we import them. We don’t make laptops. We don’t make phones, the things we use the most we don’t even make plans to establish here to make them locally and that is why exchange rate will always be a challenge to us in this country, we can’t rely on oil only for foreign exchange, we have to move out of it and in as much as government has a lot to do, some of us also have a responsibility too”

Also speaking, Mr. Bisi Oni said the recent happenings have shown that there are ways to do business afresh. He said the COVID-19 has brought new ways of doing business and has opened more opportunities.

He frowned at how the unemployment rate in Nigeria is growing drastically even at the detriment of the youth and the economy. “How would an economy grow when 35 millions of youth, people in their prime life are unemployed? It is not rocket science, you cannot wish yourself into economic growth, it has to be planned. Growth is not an accidental process, anywhere growth has happened; it takes the deliberate, conscious, and intentional process to make it work. When you see that the significant number of people that should create value in an economy or institutions are lagging, then you are headed for the rocks”

He said different policies of government are also an obstacle to economic growth. He said there should be policy harmonization and see how it should work instead of conflicting and confusing policies.

He continued that though the country is out of recession, it is momentary and volatile because it’s not sustainable until government make deliberate and coordinated programs to salvage it.

Though he said the National Bureau of Statistics (NBS) highlighted the sectors that drove the recovery to be the Agriculture, telecommunications, real estate, health and social services sector, Mr. Oni doubts if they are sustainable. He mentioned the creative sector is a promising sector that should be critically looked into because of the wide opportunities involved.

On technology, Mr. Oni said brick and mortals is not the economy of the future rather the one driven by technology service. E.g., Kuda bank a digital bank that is giving conventional banks a run for their money.

He furthered that the policy of the country is structured to resist innovation and creativity which is called for concern. “Every attempt to create something new thing is always met with resistance, either from the government, the policy or the people who are implementing it. We need a growth mindset to have sustainable growth…If the government doesn’t think sustainable growth is possible, then the people won’t follow. They need to see that trust in governance”

On diversification, Mr. Oni said there is a need to diversify the economy instead of depending on oil. According to him,“crude oil proceeds account for about two-thirds of government revenue. Yet the sector only contributes to an average of 10% of GDP yearly. In 2020 that figure was a mere 8.16% with the non-oil sector contributing 91.84%. The economy has moved, it’s high time we challenge the status quo”

On the impact of inflation on individuals, he said the inflation is at 17.3% in 5 years and the price of commodities has sky rocked and everyone is feeling the heat.

Is there a way out?

According to Mr. Oni, the structuring of personal finance is very important, the time to rethink our asset creation, strong positioning in investment as income is fixed even at this period, the need to work on our income and invest wisely.

“At this time, if you are not making money, you should not lose money and this is what will keep you through this period,”he said.

He provided alternative investment to take this time which includes Real estate, Forex, Cryptocurrency, Private equity and Crowdfunding.

He added that FundQuest Financial Services Limited is able to help individual or organisations to access some of these opportunities with multiple investment products suitable for both individuals and corporate investors.

In his own view, the chief host, Mr. Abiodun Akinjayeju said that the cumulative result of the economy we get is as a result of individual actions and the economic actors as most times we depend more on foreign but never embrace local and that is what is cumulatively affecting the GDP, exchange rate and others.

He said the structure of the Nigerian government makes it hard to make meaningful growth. “Bring angel Gabriel as president and Angel Michael has his deputy to govern Nigeria, we will fail because of the way Nigeria is structured…the Nigerian government structure is faulty, and we must admit that”. He added that until Nigeria gets the government structure right, it will be a vicious circle.

He however called on all economic actors and government to come together and make things done and the need to “think Nigeria, live Nigeria and spend Nigeria”.

The fresh injection of $51m in funding for Operations will further enhance Smile Telecoms’ position in its respective markets

Smile Telecoms Holdings Ltd., a Pan-African telecommunications group with operations in Nigeria, Uganda, Tanzania, and the Democratic Republic of the Congo, announced today, March 30th 2021 that its RP (Restructuring Plan) has been approved and agreed with the lenders.

This debt restructuring plan sees an injection in fresh money funding from Smile’s majority shareholder, the Al Nahla, and rescheduling on debt repayment until post-March 2022.

The fresh injection of $51m in funding for Operations will further enhance Smile’s position in its respective markets and energize Smile’s operations and support efforts towards achieving better performance.

Founded in 2007, with its head office in England, Smile Telecoms Holdings Ltd is a Pan-African telecommunications group with operations in Nigeria, Tanzania, Uganda and the Democratic Republic of the Congo, and South Africa. The company has one of the largest sub-1 GHz 4G LTE commercial networks in Africa, operating in the “future proof’ low band, 800 MHz band, and mid-band.

Lafarge Africa Plc (WAPCO) released its FY-2020 results last week, showing a 98.8% y/y rise in PAT to N30.8bn. Lafarge’s revenue (up 8.3% y/y to N230.6bn) grew faster than its cost of sales (up 4.0% to N163.3bn) during the period.

This, coupled with improved operating cost management (9.4% of revenue vs 9.9% in FY-2019) and a marked decline in finance costs (-51.9% y/y), resulted in a whopping 110.0% y/y increase in PBT to N34.3bn. Notably, the drop in finance costs, due to balance sheet restructuring, was again at the heart of the improvement in profitability. We review WAPCO’s latest financials, and our valuation estimates below.

Topline Performance Bolstered By Sector-Wide Demand Recovery

Following a 5.1% y/y slump in revenue in Q2-2020, which threatened the sales outlook, the easing of lockdown measures, which largely took effect in Q3 2020, supported a turnaround in WAPCO’s full-year revenue (up 8.3 % y/y to N230.6bn vs N239.8bn est.), as Cement sales (98.1% of total revenue) rose by 9.1% y/y while revenue from Aggregates and Concrete Products (1.2% of total revenue) declined by -25.5%.

WAPCO managed to keep its input costs in check, as Cost of Sales climbed moderately, in comparison to Revenue (Cost of Sales up 4.0% y/y to N163.3bn). As such Cost margin dropped 289bps y/y to 70.8% in FY-2020. Fuel and power costs (up 21.7% to N38.6bn) were mainly responsible for the increase in Cost of Sales, according to the cost breakdown.

However, the cost of materials and consumables remained stable, and lower production (down 2.6% to N23.8bn) and fixed distribution costs (down 59.3% to N1.8bn) helped alleviate cost pressures, as shown by the increase in Gross Margin (29.2% in FY-2020 vs 26.3% in FY-2019).

EBITDA was up 16.0% on the back of turnaround initiatives vis-à-vis WAPCO’s “Health, Cost and Cash” strategy to cut down on excessive operating expenses, which climbed by 2.5% y/y to N21.5bn.

Specifically, the company curtailed Selling and Marketing expenses (down -17.2% to 4.2bn), as advertising, campaign and innovation expenses fell dramatically. This offset increases in Directors costs (up 391.4% to N174.3m) and staffrelated expenses (up 15% to N6.2bn). This made for a decent operating performance as the company posted a 217bps increase in EBITDA margin to 32.7%.

Balance Sheet Improvements Drive Finance Costs Lower, Prop Up Net Income

WAPCO sustained its efforts in deleveraging its balance sheet as Total Debt declined by 22.5% y/y to N49.7bn. Notably, the company’s Debt to Total Capital ratio improved to 0.41x (from 0.44x in FY-19 and a 1.76x 5-year average). Consequently, Net finance cost tumbled 49.9% y/y, driven by a 51.9% drop in interest expense to N9.7bn, further aided by the low-interest rate environment. As a result, Pre-tax profit surged 110.0% y/y to N37.6bn while Post-tax profit grew 98.8% y/y to N30.8bn.

Additionally, effective working capital management, particularly in terms of inventories (inventory turnover of 5.1x vs 4.0x in FY-2019) and trade receivables (receivables turnover of 7.3x vs 5.4x in FY-2019), aided cash generation (Cash and cash equivalents grew 96.7% to N53.3bn).

Looking ahead, we are cautiously optimistic about WAPCO. Although we expect continued revenue growth driven by broader demand trends and economic momentum, which should drive higher volumes.

The company’s operational difficulties (particularly in its Ewekoro and Mfamosing plants), which were mostly illustrated in its Q4-2020 performance (revenue rose by just 1.5% y/y), weigh slightly on our outlook. Specifically, we have forecasted a 9.0% y/y growth in Revenue as we expect a stronger outing in FY-2021 hinged on management guidance on the resolution of the operating challenges experienced in Q4-2020 which capped revenue growth. On the cost level, we expect the company’s cost optimization strategies to bear more fruit, and input costs to normalize later in the year, allowing for margin improvement. However, we express our concerns over the depressed marketing spend, considering competitors’ marketing strategies and the intensifying competition for market share. In all, we estimate a 16.9%y/y improvement in EPS to N2.2/share.

Adjusting our model estimates for the new assumptions, higher risk-free rate and country risk premium, we review our year-end target price downward to N27.7/share, from N32.5/ share. The stock’s current market price of N22.25/share reflects a 24.3% discount to our year-end Target Price. Also, the counter currently trades at a P/E of 11.6x, compared with domestic peers, DANGCEM (13.9x) and BUACEMENT (35.3x). Thus, we maintain our BUY rating on the ticker.

Recently, the CBN in its Monetary Policy Committee (MPC) meeting communique, revealed Nigeria’s Purchasing Managers Index (PMI) for the months of January and February 2021.

According to the numbers, economic activities remained below the expansion threshold of 50pts during the survey period.

This was true for the Manufacturing and Non-manufacturing, indices. However, a month-on-month analysis indicated that both manufacturing and non-manufacturing economic activities improved significantly, from 44.9pts and 43.3pts in Jan-2021 to 48.7pts apiece in Feb-2021.

The MPC communique also revealed that the Employment level component of the Manufacturing and Non-manufacturing PMIs increased to 45.6 and 48.0 index points, respectively, from 44.2 and 45.0 index points in the prior month.

Clearly, the weakness across the purchasing manager’s indices indicates that economic activities within the country are yet to recover to their pre-COVID-19 levels. Certainly, economic recovery is underway, considering the rebound in economic activities observed in Q4-2020 and the scale of reopening of the economy since the great lockdown of 2020.

However, the sub-50pts PMI reading between Jan-2021 and Feb-2021, foreshadows a muted growth outlook for Q1-2021, if history is anything to go by.

For context, the manufacturing sector is heavily reliant on FX availability (but the FX market remains largely illiquid) and increased consumer welfare, which appears to still be in a puddle. Overall, our forecast for GDP growth in Q1-2021 is a mild y/y expansion at best, as seen in Q4-2020, considering the base-effect of Q1-2020 (+1.9% y/y), given that the Covid-19 pandemic had not surfaced as at then.

In 2020FY, Dangote Cement Plc. proved its mettle as it continued on the path of growth and like we expected, reached a revenue milestone.

The company was unhindered by challenges from the COVID-19 pandemic as seen in the impressive year-on-year performance recorded in its home market and some pan-African locations.

In Nigeria, the low interest rate environment in 2020 made an investment case for the real estate sector and as such, propped up cement demand.

With support from its national consumer promotion (bag of goodies season 2) programmme, DANGCEM continued to enjoy significant market share. Thus, the company sold 15,739 Kilotons of cement in Nigeria in 2020FY (up 11.47% YoY). Also, adding to the success of its maiden clinker export in June, the company pushed out six more vessels via its Apapa terminal and continued cement exports by road.

Hence, total export volumes for the year amounted to 197 Kilotons. Overall, its Nigerian operations could boast of a total sales volume of 15,936 Kilotons (vs 14,119 Kilotons in 2019FY), which earned the company a revenue of NGN719.95 bn (vs NGN610.25bn in 2019FY).

Giant strides were also recorded in some of its Pan-African operations, with Congo leading the pack with a 59.00% increase in sales volume and Senegal at full capacity utilization. Other Pan-African businesses also performed better year-on-year, with the exception of Zambia and Ghana where sales volumes declined.

Consequently, Group sales volumes for the year was 25,721 Kilotons – an increase of 8.61% YoY. Thus, the company’s total revenue grew by 15.98% to NGN1.03trn (vs optimism stems from the continued adoption of cement for road construction and higher export volumes (on the back of the recently reopened borders and AfCFTA).

Profitability Undeterred by Heavier Tax Burden

Although energy costs spiked by 19.12% (an offshoot of the Naira devaluations) in 2020, cost-to sales ratio was marginally lower at 42.35% (vs 42.62% in 2019FY) as the increase in the cost of sales only played catch-up to revenue performance.

In a similar vein, improved logistics management which yielded a decline in haulage expenses (-7.67% YoY) ensured a moderation in operating expenses (-0.33%) despite higher administrative costs (+11.48%). EBITDA thereby increased by 16.67% to NGN421.42bn (vs 361.20bn in 2019). Furthermore, a combination of higher interest income (+76.23%) and foreign exchange gains of NGN16.63bn contributed to the increase in Profit before tax by 49.04% to NGN373.31bn.

We note also that the expiration of the pioneer tax status on most of the company’s plants in 2020 resulted in a higher effective tax rate of 26.05% (vs 19.94% in 2020FY). Nonetheless, Profit after tax (NGN276.07bn) bettered the previous year’s performance (NGN200.52bn) by 37.68%. This put the company’s net margin at 26.69% (vs 22.49% in 2019FY).

In the last quarter of the year, the company completed the first tranche of its share buyback programme, recalling 0.24% of its shares outstanding. While this did not significantly impact its share price, a combination of stronger earnings gave EPS a lift to settle at NGN16.14 (vs NGN11.79 in 2019) .

Recommendation

In arriving at our 2021FY target price, we project an EBITDA of NGN556.93.bn and an EV/EBITDA of 7.83x. Having adjusted for an expected net debt of NGN406.19bn, we arrived at a target price of NGN232.64, an upside potential of 3.86% when compared to its closing price of NGN224.00 on March 29, 2021.

The year 2021 has started off on a high note for electric vehicle (EV) funding and it seems set to break the previous year’s records.

According to the research data analyzed and published by ComprarAcciones.com, the month of January 2021 alone saw funding deals worth approximately $6.45 billion in the industry. These included SPAC mergers, IPOs, funding and acquisitions.

2020 set off a new trend for electric vehicle (EV) companies, many opting to go public via Special Purpose Acquisition Companies (SPACs). Among the key EV names that took this route were Nikola, Hyliion Holdings, Fisker, Lordstown Motors and QuantumScape.

Based on Bank of America’s projection, the transition towards full vehicle electrification might cost more than $2.5 trillion in global investment over the coming decade. SPACs are just one of the ways to raise the required capital.

In January 2021, EV charging network EVgo announced a merger with Climate Change Crises SPAC. Based on the terms of the deal, EVgo would receive $575 million from the merger. Under the deal, which is set to close in Q2 2021, the combined company value would be $2.6 billion.

Electric bus maker Proterra also announced a SPAC merger with ArcLight Clean Transition Corp. The transaction is set to raise $825 million and the enterprise value will be $1.6 billion once it closes in H1 2021.

Meanwhile, battery cells developer FREYR announced a SPAC merger with Alussa Energy Acquisition Corp. It will receive $850 million in equity proceeds and the combined company will be worth about $1.4 billion.

Global Electric Vehicle Market to Grow at 10.6% CAGR to $236 Billion by 2027

Other January 2021 deals include Faraday Future’s merger with Property Solutions Acquisition ($750 million) and Lucid Motors deal with Churchill Capital IV (CCIV).

There had been a nearly fivefold increase in share price since January when reports of the anticipated Lucid Motors – CCIV deal began circulating. Following the merger announcement however, shares of the latter took a 38.6% plunge.

In February 2021, Volta Industries, which is another charging station network, announced a SPAC merger with Tortoise Acquisition Corp II. Valued at $2 billion, the deal will rake in $600 million for Volta.

Additionally, electric truck startup Xos also struck a $2 billion deal during the month with NextGen Acquisition Corp. It expects to receive $575 million in proceeds from the merger. Battery maker Microvast agreed to a merger with Tuscan SPAC in a deal that will value the combined entity at about $3 billion. It will receive $822 million in cash proceeds following the merger.

The massive upsurge in EV SPACs and capital raises comes as no surprise in view of anticipated demand. In the US, for instance, the President announced plans to replace the entire federal fleet of vehicles with EVs. That is a total of 645,047 vehicles. Shanghai, on the other hand, plans to have EVs account for 50% of all new vehicle purchases by 2025. By that time, all its public buses, delivery trucks, taxis and government vehicles will be electric.

According to analytics firm Blastpoint, there was an increase of 30% in US EV sales in 2020. In 2021, sales are projected to rise by 71%. Analysts state that 2021 will be a pivotal year for the US EV market with a deluge of new models making an entry. From 17 models in 2020, the figure will rise to 30 models.

The global electric vehicle market was worth $121.8 billion in 2020. It is set to grow at a 10.6% compound annual growth rate (CAGR) over the period between 2021 and 2027, to about $236.3 billion.

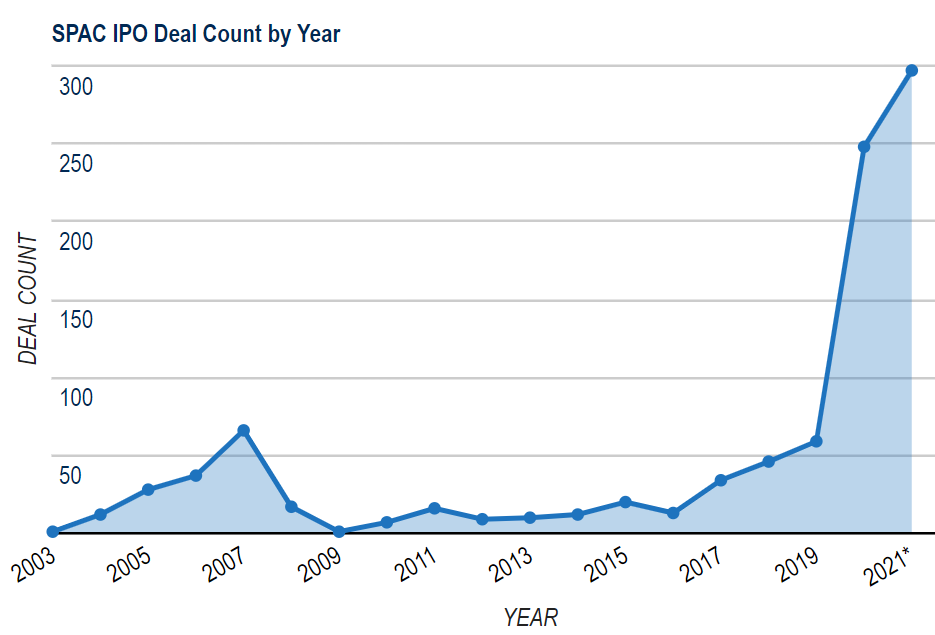

145 SPACS Raised $44.5 Billion by Mid-February vs. 55 Traditional IPOs Valued at $21.7 Billion

The 2021 SPAC boom is not limited to the EV industry alone. Based on data from SPAC Insider, 145 SPAC IPOs had raised a collective $44.5 billion+ this year as of February 17, 2021. According to the research firm, average deal size at the time was $307 million.

Comparatively, there had only been 55 traditional IPOs during that time, having raised $21.7 billion according to Renaissance Capital.

For perspective, there were 248 SPAC IPOs in 2020, which raised a cumulative $83 billion. That was over six times the amount raised in 2019 and four times the total IPO value in 2019. As of mid-February 2021, SPACs outnumbered IPOs nearly 2-to-1.

However, the rate at which these blank check companies are pricing is higher than the pace at which they are finding targets. At the time, only 43 out of the 145 SPACs had announced merger targets.

Americans are losing billions due to internet crime each year. However, 2020 was a record year for both the cybercrime victims and the combined financial losses caused by these malicious attacks.

According to data presented by Stock Apps, the total annual loss of cybercrime in the United States hit $4.2bn in 2020, a 55% increase in two years.

Business Email Compromise Schemes Caused 40% of Total Cybercrime Losses

Cybercrime costs include damage and destruction of data, stolen money, theft of intellectual property, personal and financial data at slots sites, post-attack disruption to the normal course of business, restoration of hacked data and systems, and reputational harm.

In 2005, the combined financial loss caused by cyber-attacks and frauds amounted to $183.1 million, revealed the FBI’s 2020 Internet Crime Report. By the end of 2011, this figure soared by 165% to $485 million and continued rising.

In 2015, the total financial damage caused by cybercrimes in the United States hit $1bn for the first time, but that was just the start of its massive growth. By 2019, this figure tripled and hit $3.5bn. Last year, almost 792,000 complaints were logged by the FBI’s Internet Crime Complaint Center (IC3), with total losses jumping by 20% YoY to $4.2bn.

Statistics show phishing attacks, non-payment scams, and extortion were the most frequent internet crimes in the United States. However, business email compromise schemes were the costliest cybercrimes, causing $1.8bn or 42% of total losses last year.

The IC3 report showed last year also witnessed a number of cyber schemes exploiting the COVID-19 pandemic with both individuals and businesses targeted. More than 28,500 received complaints related to COVID-19 scams, and most of them aimed at the Coronavirus Aid, Relief, and Economic Security Act. Many Americans were also scammed to provide personal information in exchange for vaccination appointments.

Cyberterrorism the Biggest Potential Threat to the United States

Over the years, the United States has had to cope with a long list of threats, from geopolitical tensions with China and Russia to international terrorism and the spread of infectious diseases. Ultimately, the COVID-19 outbreak emerged as one of the countries of the most serious threat ever faced.

Despite that, the pandemic is not viewed as the biggest threat to the United States by the public. According to a Gallup survey, cyberterrorism is viewed as the top threat by Americans. More than 80% of respondents named it the most critical threat the country will face over the next decade.

The development of nuclear weapons by North Korea and Iran ranked second and third on the threat list, while international terrorism and infectious diseases were tied in fourth place.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.